From carbon neutrality roadmaps to reality

Holcim Germany

Holcim Germany

S&P Gobal

S&P Gobal

S&P Gobal

S&P Gobal

S&P Global

S&P Global

S&P Global

S&P Global

VDZ

VDZ

GCCA

GCCA

Cembureau

Cembureau

IEA, [9]

IEA, [9]

HeidelbergCement

HeidelbergCement

Holcim Deutschland

Holcim Deutschland

[10]

[10]

[15]

[15]

[16]

[16]

Bildquelle Re magnis denda abo. Namenim agnatqu id

Bildquelle Re magnis denda abo. Namenim agnatqu id

tkIS

tkIS

The cement industry is on a transformation path towards carbon neutrality. Several roadmaps have been developed to outline the opportunities, challenges and actions to reach this goal. However, almost never have the risks of such a transformation been described and neither have the resources and costs that are necessary to achieve the goals. Accordingly, the question is, how can the roadmaps become reality? This article provides some answers.

1 Introduction

Carbon neutrality roadmaps 2050 are provided by a number of industries such as energy, iron & steel and cement. There are also roadmaps by governments such as the European Union (EU), organisations such as the United Nations (UN) or independent conservation organizations such as the World Wildlife Fund (WWF). The main purpose of the industry roadmaps is to contribute to the goal of limiting the global warming to a level well below 2 °C (preferably to 1.5 °C) by mid-century, when compared to pre-industrial levels (COP 21, Paris agreement, adopted Dec. 2015). However, the latest UN climate report [1] has attested that the world is steering towards global warming of 2.7 °C by the year 2100 and the governments have missed their mark. In its current analysis [2], the Intergovernmental Panel on Climate Change (IPCC) expects that the critical mark of 1.5 °C will probably already be reached in 2030.

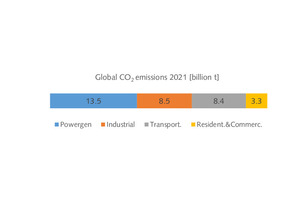

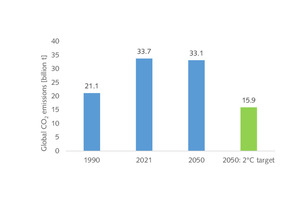

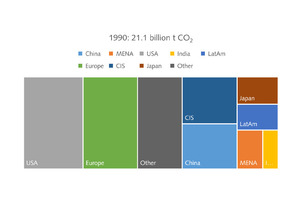

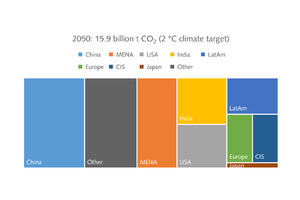

According to S&P Global Market Intelligence [3], the global manmade CO2 emissions excl. agriculture were about 33.7 billion t in 2021, of which 13.5 billion t were from power generation and 8.5 billion t were from the industrial sites (Figure 1). The CO2 emissions increased from 15.1 billion t in 1990 and will be still around 33.1 billion t in 2050, according to the S&P reference projections (Figure 2). The target for 2050 should be only 15.9 billion t to hit the 2 °C target. In Figure 3 the world regions are compared to each other in terms of their CO2 emissions in 1990 and 2050 (target). The shift from developed to developing world regions is obvious. Western Europe and the USA made up a small amount of emission reductions over the past decade. Even if these regions achieve zero emissions the rest of the world would still need to decline by 65% from current levels by 2050.

2 Roadmaps by the cement industry

In 2009, the International Energy Agency (IEA) and the Cement Sustainability Initiative (CSI) of the World Business Council for Sustainable Development (WBCSD) formed a partnership to jointly produce the first industry-specific roadmap, entitled Cement Technology Roadmap 2009 [4]. This roadmap was updated in 2018 and also a number of other cement industry roadmaps were published e.g. by Cembureau, the European Cement Association [5], GCCA (Global Cement & Concrete Association) [6], the PCA (Portland Cement Association and the VDZ (German Cement Association, to name a few. The VDZ was also one of the first institutions in the cement industry to publish a roadmap on the future resources for cement and concrete [7]. The consumption of resources is responsible for a large part of global warming.

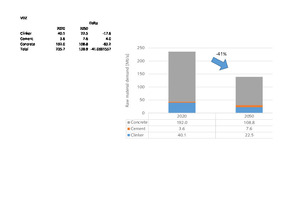

The VDZ published a scenario 2050 [7] on the reduction of primary raw materials along the value chain of cement and concrete. According to this study, with 12% lower construction demand and a development in concrete construction, it would be possible in Germany to reduce the consumption of primary raw materials, such as limestone, gravel and natural stone, by about 41% (Figure 4). The largest potential in saving natural resources is in the concrete production, with 83.2 million annual t (Mt/a), mainly by the use of recycled materials obtained from the demolition of buildings. Raw materials for clinker production can be reduced by 17.6 Mt/a by reducing the clinker factor from 71% in 2020 to 63% in 2030 and 53% by 2050, even with a lower availability of granulated blast furnace slag and fly ash. But the raw material demand for cement production will increase by 4.0 Mt/a, especially because of the increasing quantities of limestone and calcined clays needed for the reduction of the clinker factor.

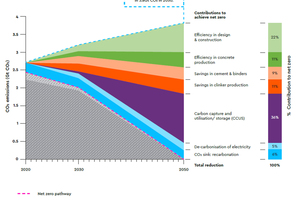

According to the Global Cement and Concrete Association (GCCA), in 2020, about 4.2 billion tons of cement and 14 billion m3 of concrete were produced worldwide [6], while the market value of global cement and concrete products was US$ 440 billion. However, the total global CO2 emissions from the sector were about 2.7 Gt and this is forecast to increase to 3.8 Gt CO2 by 2050 in the absence of any actions (Figure 5). The emissions are primarily direct CO2 emissions from clinker production, which in turn are from limestone decomposition (approx. 60%), while combustion of fuels, electricity use and other cement and concrete plant processes are responsible for the remaining 40%. Given this situation, it sounds very unrealistic that these emissions could be reduced to zero with a higher efficiency in concrete production (-11%) and a higher efficiency in design and construction (-22%). Should cement and concrete production not better be separated to make the process more transparent?

The roadmap “Cementing the European Green Deal” [5], that was presented by Cembureau in 2020 only took into consideration the emission savings that the cement industry could achieve to reduce its own emissions. In 1990, the average emissions of 783 kg CO2/t cement in 2017 had already been reduced by 116 kg CO2/t cement (or 15%) (Figure 6). While their first Roadmap (elaborated in 2013) set an 80% CO2 reduction target, the new Roadmap is aiming for a complete carbon neutrality by 2050. This shall be achieved with the “5C approach” that promotes a collaborative approach along the clinker-cement-concrete construction-carbonation value chain to turn the low carbon vision into reality. The intermediate goal by 2030 is to achieve emissions of 472 kg CO2/t cement down the value chain.

Cembureau envisages up to a 3.5% reduction in process CO2 using decarbonated materials by 2030 and aims to reach 60% alternative fuels containing 30% biomass plus a 4% improvement in thermal efficiency by 2030. This is very much in line with the carbon neutrality targets of the major cement producers in Europe. They are striving to increase the use of alternative raw materials and fuels, substitute the CO2-intensive clinker in cement with secondary cementitious materials that have a significantly lower CO2 footprint and increase plant efficiency and CO2 reduction at plant level by major investments. One goal is to upgrade plants with the latest dry calcination technology and to implement Carbon Capture, Storage and Utilisation (CCUS) technologies [8]. After 2030, the CCUS technologies will have the major impact on the reduction of carbon emissions.

3 Cost & risks analysis

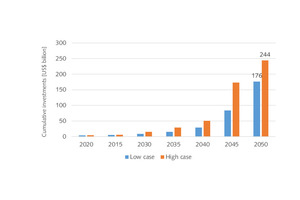

In their roadmap in 2018 the IEA came up with estimates for investment costs for the global cement industry to achieve a Reference Technology Scenario (RTS) of limiting the global warming to below 2.7 °C in 2100 and a Roadmap vision of limiting the global warming to well below 2 °C (2DS). In the RTS scenario about 7 Mt/a CO2 have to be removed by CCUS technologies by 2030 and 83 Mt CO2 by 2050, while in the 2DS scenario these cuts have to be 14 Mt CO2 by 2030 and 552 Mt CO2 by 2050. However, the estimated costs for the CCUS technologies have been shocking (Figure 7). The IEA came to the conclusion that between US$ 176 to 244 billion cumulative investments are necessary to achieve the 2DS roadmap vision, even excluding CO2 transport and storage costs [9]. These cumulative investments are really huge when compared to the annual global Capex of the cement industry of around US$ 8-9 billion.

With today’s knowledge it is certain that CCUS technologies can be provided with competitive costs. The lowest carbon avoidance costs are offered by direct separation and oxyfuel combustion. In the direct separation process, a special reactor replaces the conventional calciner to separate the process CO2 from the limestone calcination. The technology is based on an indirect heating of the cement raw material via a special steel tube within the calciner (Figure 8). The advantage is that the pure process CO2 can be captured as it is decomposed from the CaCO3, while the furnace exhaust gases are kept separate. The system can be applied to existing and new kilns and the carbon capture requires no additional use of heat or any other commodities.

In the Leilac direct separation system the lowest CO2 avoidance costs are given as 37 €/t CO2 for a new plant and 38 €/t CO2 for a retrofit of a cement kiln with 1 Mt/a capacity [10], depending on the configuration.

In the oxyfuel method, pure oxygen replaces ambient air in the clinker production process. There are already several projects under development (Figure 9). As the nitrogen content of the air is no longer present, the CO2 concentration in the kiln exhaust gas can be increased up to 100%. Accordingly, an efficient CO2 separation can be used for the downstream utilisation or storage of carbon dioxide. In the 2nd generation of oxyfuel systems, complex exhaust gas recirculation is completely eliminated [11]. The gas volume in the clinker burning process is considerably reduced. For cement producers, the 2nd generation will allow reduced investment and operating costs. CO2 abatement costs have been stated by [12], probably based on ECRA (European Cement Research Academy) estimations as 70 to 131 €/t CO2 by 2030 and 65 to 87 €/t by 2050.

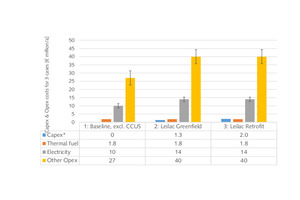

At the moment the “Costs of CO2 avoidance” calculations by the Leilac set the benchmark for the decarbonisation of the cement industry. A direct calcination system for a 1 Mt/a cement plant fuelled by RDF will typically capture 489 kt CO2/y, which corresponds to a 63% CO2 emission reduction. The capital costs for the installation of a greenfield plant are in the range of € 58 to 64 million, and for a retrofit installation € 66 to 77 million. The net additional Capex above an unabated reference plant is around € 27-34 million for a greenfield plant, and € 34-44 million for a retrofit. Figure 10 shows the calculated annualized Capex and Opex costs for a Leilac system for the low-cost case, compared to a baseline plant with no CO2 reduction. The results are low “Costs of CO2 avoidance” of 37 and 38 €/t CO2, of which the capture process only needs 12 and 14 €/t CO2 [10].

The transition to carbon neutrality is full of risks and will require not only efforts from the industry but also from external stakeholders, policy makers and consumers. Accordingly, the cement industry will need access to raw materials, by-products, waste fuels, renewable energy and a proper regulatory framework that allows investments against reasonable returns. The investments in carbon abatement technologies will significantly increase Capex and Opex costs of cement production and cement prices will increase due to CO2 abatement. Therefore, policy makers have to assure that a fair competition is possible between cement producers investing in CO2 abatement and others not investing in these technologies. Asymmetry raises the fear of carbon leakage – a shift of cement production and CO2 emissions from a region with emission constraints to an unregulated region.

CCUS is a cornerstone of the net zero carbon roadmap for the cement industry. However, CCUS technologies can only be successful if the infrastructure allows the transport, re-use and storage of the CO2 it captures. The policy makers have to support the development and implementation of a CO2 transportation network that responds to the industry’s needs. An essential part of this will be the re-evaluation of CO2 as a usable commodity rather than a waste product. Captured CO2 can be used in the production of e-fuels or as a feedstock for the chemical industry. The problem is, these possibilities are still far away from being economical. Another opportunity is the utilisation of captured CO2 within the cement and concrete industry such as injection into wet concrete and the curing of hardened concrete.

4 The policy challenge

Some experts are coming to the conclusion that the free allocation of CO2 emissions for the cement industry by the European Union Emissions Trading System (EU ETS) has been a failure, because the companies had no incentive to develop CCUS technologies [13]. Instead, because of large cement overcapacities in the period from 2008-2019, the cement industry made windfall profits of € 10.3 billion from selling the surplus allowances on the carbon market, without being subject to any pre-conditions to spend this money on future climate action. Meanwhile, the cement industry and other energy-intensive industries in the EU, deemed responsible for “carbon-leakage”, still receive most of their allowances for free. A provisional agreement in Dec 2022 on reform of the EU’s emission trading system foresees a phasing out of free carbon allowances over a nine-year period between 2026 and 2034, allowing for the gradual introduction of the Carbon Border Adjustment Mechanism (CBAM).

For Cembureau it is indispensable to ensure that a CBAM effectively equalises CO2 costs between EU and non-EU suppliers before any phase-out of free allocation is initiated. In particular, the CBAM has to [14]:

Ensure a full CO2 cost equalisation by strictly mirroring the carbon costs faced by EU suppliers

Develop a watertight monitoring and reporting system for measuring embedded emissions and avoiding circumvention

Include indirect emissions (electricity) and give due consideration to transport emissions, thereby mirroring the CO2 cost structure of EU producers

Include a solution for EU exports to avoid a situation where CBAM would result in lower access to export markets for the European industry, with a negative impact on global CO2 performance

Ensure that CBAM comes into operation as soon as possible to mitigate the risk of carbon leakage which is increasing under the pressure of growing imports, changing import business patterns and a sharp increase of the CO2 price

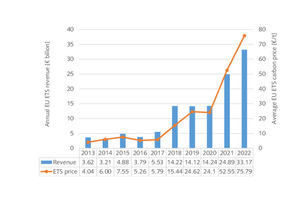

Figure 11 shows the annual EU ETS auction revenues and the corresponding ETS carbon prices [15]. In the last few years the ETS carbon prices have sharply increased from an average price of about 14 €/t CO2 to more than 70 €/t CO2. The EU member states were able to raise € 88.5 billion in ETS revenues in the period from 2013 to 2021. In that period another € 98.5 billion were given as free allowances. If these free allowances had been auctioned, the revenues could have more than doubled. Anyhow, since the purpose of the ETS is to reduce carbon emissions, it is only logical that the revenue generated by the carbon price be spent on climate action projects. However, according to Member State reports, only 71.9% of ETS revenue collected between 2013-2021 was spent on climate action. This definitely needs to be improved in future.

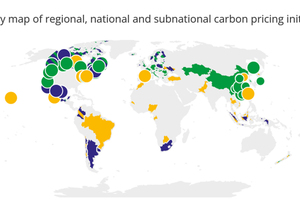

According to the latest report by the Worldbank’s annual “State and Trends of Carbon Pricing” [16] global carbon pricing revenue in 2021 rose to around US$ 84 billion, which is an increase by almost 60% from 2020 levels. The revenues provide an important source of funds to help support a sustainable economic recovery, finance broader fiscal reforms, or invest in communities as part of the low-carbon transition future. The report, which presents the latest carbon pricing developments around the world, finds that there are 68 direct carbon pricing instruments operating today (Figure 12): 36 carbon taxes and 32 Emissions Trading Systems (ETS). Four new carbon pricing instruments have been implemented since the release of the 2021 State and Trends of Carbon Pricing report: one in Uruguay and three in North America (Ontario, Oregon, New Brunswick). Countries announcing plans for new carbon pricing policies include Israel, Malaysia and Botswana.

The list of required governmental measures is long and concern not only an adequate and fair carbon emissions trading system. Achievements on carbon neutrality and on a circular economy will not come easily and will require technology advancements, regulatory refinements, new ways of thinking about clean energy and industrial fuels, and increased resiliency of our buildings and infrastructure. In many regions it will also be difficult to significantly reduce the clinker ratio in cement (Figure 13), due to a reduced availability of by-products such as granulated blast furnace slag and fly ash. A more circular approach to by-products and buildings is key to the reduction of emissions. Policies should maximise the different properties of construction materials, including their durability, recyclability, thermal mass or re-carbonation potential.

5 Outlook

The cement industry will be responsible for the necessary investments to achieve carbon neutrality. Governments are able to support these investments with funds from the ETS revenues. However, it is required that the companies have a reasonable return on their investments and that enough cash flow is generated from the operations to make investments possible. This will not be the case for all cement producers, especially those which have high net debt and/or suffer low profit margins and run cement plants with an age of 50 years and more. In Western Europe alone it is estimated that due to large overcapacities about 10 to 15% of the cement plants will fall under these categories and are in danger of being phased-out. Accordingly, thousands of job losses will result, although these will be at least partly compensated by new job creations in the carbon reduction market.