Cement industry joins growth trend

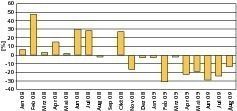

The strong upswing of the overall economic trend has also had a positive effect on the German cement industry. With the recovery of the overall economy, developments in the building markets are slowly becoming more promising again. This is based on the provisional figures of the cement branch as regards the turnover and cement consumption in 2010 as well as on the outlook for the next year. However, in the first quarter of the year, the cement manufacturers as well as the entire building trade had to face a severe decline in production. After it was possible to compensate for these losses to a great extent in the course of the year, the cement industry is gradually making up for these setbacks. “High hopes are placed in policy makers to create the financial and infrastructural conditions to make it possible for the building and building materials industries to play an active role in the growth trend”, underlined Dr. Martin Schneider (Fig.), general manager of the Federal German Association of the Cement Industry (BDZ), when he presented the current figures. In the wake of the strong increase in the GDP by almost 4 % in 2010, the cement consumption in Germany with probably about 25 million tons this year will become stable at the level of last year. Due to this positive trend and the promising signs in particular as regards residential building and commercial buildings, the branch expects a growth of 2.2 % in 2011.

The turnover of the cement branch dropped slightly by approx. 3.4 % in the first nine months of 2010. However, the companies in the cement branch maintained the employment picture with 7343 employees at a stable level to a great extent. In the first three quarters the foreign trade, both exports and imports, was more or less maintained at the level of the previous year.

At present, the construction industry is quite different in the individual segments. While residential building, starting from a low level, exhibits a clear upward trend and the incoming orders for commercial buildings have clearly increased, the situation in road construction in particular is problematic. Though the capital for federal roads was clearly increased due to the economic stimulus packages, obviously capital spending, above all of the municipalities, is on the decrease in this segment. Schneider: “From 2011 it is feared that also public building construction will be affected when the economic stimulus programs come to an end.”

For home building alone the BDZ expects an increase in cement consumption of about 10 % for 2010. For 2011 a slightly weakened recovery in East Germany is expected (+3 %) and a stable positive upward surge in West Germany (+9 %). A recovery is also expected for multi-storey residential building. Here, the branch expects a growth in cement demand of about 8 %. In the meantime the construction of non-residential buildings has clearly developed better after the massive drops due to the economic crisis in the past, so that a change in trend can also increasingly be expected. While the BDZ expects drops in cement demand of about 12 % for industrial buildings in 2010, they already expect a growth of about 8 % for 2011.

In contrast, developments in civil engineering overall are estimated critically in the branch. Certainly a growth rate of 1 % to 2 % is still possible in 2010 due to the positive development of incoming orders in road construction in 2009. However, as a whole they expect risks as regards the financing of public civil engineering after 2010. Schneider: “The medium-term to long-term financing of the federal roads is still not clear despite the high requirement for construction and the growth to be expected, in particular, in goods transport.” The public investment delay may only be overcome by changing the financing of the roads from budgetary to user financing as well as by an increased mobilization of private capital and private know-how. The complete project tying of the truck toll from 2011, as planned by the federal government, would be an important step in the right direction, explained Schneider.