Availability of cement raw materials

HeidelbergCement

HeidelbergCement

British Geological Survey

British Geological Survey

VDZ

VDZ

![3 Global cement and clinker production outlook [2]](/uploads/images/2022/w300_h200_x421_y297_Harder_RawMaterials_Figure_3-498da002e28ad741.jpeg)

OneStone Consulting

OneStone Consulting

![5 Limestone imports in India [4]](/uploads/images/2022/w300_h200_x421_y297_Harder_RawMaterials_Figure_5-625b5ff775901e5c.jpeg)

![6 Limestone reserves in India 2015 [4]](/uploads/images/2022/w300_h200_x421_y297_Harder_RawMaterials_Figure_6-745fb1e0d6d9c009.jpeg)

![7 Limestone reserves in S.-Korea and Vietnam [5]](/uploads/images/2022/w300_h200_x421_y297_Harder_RawMaterials_Figure_7-8c89a4a177b5b7d2.jpeg)

UltraTech Cement

UltraTech Cement

Holcim

Holcim

![10 Cement production outlook [2]](/uploads/images/2022/w300_h200_x421_y297_Harder_RawMaterials_Figure_10-ccb432124bc1c91b.jpeg)

![11 Clinker production and cement additions [2]](/uploads/images/2022/w300_h200_x421_y297_Harder_RawMaterials_Figure_11-24c40545dabf65cd.jpeg)

VDZ

VDZ

VDZ

VDZ

![14 Global GBFS production outlook [6]](/uploads/images/2022/w300_h200_x517_y330_Bild2-da046e45fd39cd69.jpeg)

OneStone Consulting

OneStone Consulting

![16 New coal-fired power plant capacity [7]](/uploads/images/2022/w300_h200_x421_y297_Harder_RawMaterials_Figure_16-e7cc9c2eaaa5aefc.jpeg)

![17 Retired coal-fired power plant capacity [7]](/uploads/images/2022/w300_h200_x421_y297_Harder_RawMaterials_Figure_17-750395caa9cf754b.jpeg)

OneStone Consulting

OneStone Consulting

OneStone Consulting

OneStone Consulting

Cement plants with capacities of 1 million t per year consume 1.5 million t of raw materials, which corresponds to almost 5000 t/d, and this over a period of at least 40 years. Most of the raw materials are for the clinker manufacturing, but depending on the clinker factor large quantities of cement additives are also required. This article provides a review of the availability of cement raw materials and of the latest trends.

1 Introduction

The fundamental requirement for the manufacture of cement clinker is adequate sources of lime (CaO), silica, alumina and iron oxide. The optimal composition of the four main oxides is governed by the LSF (Lime Saturation Factor), which controls the ratio of the primary clinker phases of alite to belite, the silica modulus, which controls calcium silicates, and the alumina modulus, which determines the relative proportions of aluminate and ferrite phases in the clinker. Typical LFS values of modern clinkers are 0.92 to 0.98 and require a cement-grade limestone as the primary raw material. Beside limestone, other primary raw materials are marl, chalk, clay and claystone, gypsum, sand and small quantities of iron ore. The availability of raw materials is the determining factor in the location of cement plants (Figure 1) and accordingly they are mostly located in close proximity to huge limestone or marl deposits.

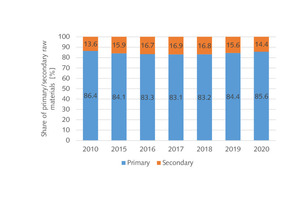

Table 1 shows the quantities of the required raw materials for the German cement production. In 2019 a total of 34.185 million t per year (Mt/a) of cement were produced, for which in total 51.145 Mt/a of raw materials (excl. fuels) were required. 43.117 Mt/a were primary raw materials, of which alone 39.554 Mt/a or 91.7% were limestone, marl or chalk to provide the lime component [1]. 7.968 Mt/a of secondary raw materials were used, of which 7.020 Mt/a was granulated blast furnace slag (GBFS), a by-product of the steel industry. Relatively very low quantities of fly ash have been used by the German cement industry, because in Germany and many other western countries the preferred use of fly ash is as an additive to concrete. FGD-gypsum, which like fly ash is also a by-product of coal-fired power generation, has been used in relatively low amounts as a substitute for natural gypsum and anhydrite, which are used as a retarder for cement.

Figure 2 is an analysis of the use of secondary raw materials in the German cement industry over the last decade. The lowest secondary material rates were in 2010 with only 13.6%. Then the rate increased to 16.9% in 2017 and since 2017 the secondary raw material rate has been declining. This has mainly to do with the availability of by-products from other industries, including GBFS, fly ash and FGD-gypsum. In Germany the proportion of CEM I cement in 2019 was 27.4%, that of CEM II /S /P / V was 19.3%, that of CEM II / T /LL /M was 29.8%, that of CEM III was 22.6% and that of CEM IV and CEM V was only 0.9%, while the clinker/cement ratio (clinker factor) was 0.71, which is close to the global level. However, the global clinker factor increased from 0.70 in 2019 to 0.72 in 2021, although most of the future scenarios suggest that the clinker factor will further decline.

2 Clinker manufacturing

2.1 Market trends

Figure 3 shows the global clinker and cement production development over the last few years with an outlook to 2025 and 2030 [2]. It is projected that the clinker and cement production will peak in 2021, mainly due to the decline in China’s cement demand in the coming years. The clinker/cement ratio is also projected to peak in 2021, due the ongoing decarbonisation efforts of the cement industry and the increasing use of clinker substitutes. Accordingly, one effect is that clinker production will decline faster than cement production, which not only has an effect on the CO2-emissions of the cement industry but also on the demand for clinker raw materials. However, the projections for the demand for limestone should not only take the demand for clinker manufacturing into account, but also the limestone demand as a clinker substitute in CEM /LL cements, as well as the increasing demand for LC3 cements. This means that in future the demand for limestone could even increase.

2.2 Availability of limestone

Limestone is a common type of carbonate sedimentary rock. It is composed mostly of the minerals calcite and aragonite, which are different crystal forms of calcium carbonate (CaCO3) and also contains SiO2, Al2O3, Fe2O3 and other elements such as sulphur and chloride impurities. In almost all countries, limestone is found in significant, economically viable volumes (Figure 4). It is estimated that the world production of limestone is in the order of 6.5 billion t per year. This figure includes limestone used as building stone, gravel and aggregate, as well as limestone used in the cement, lime, iron & steel, chemical, environmental and agricultural industries. However, it has to be noted that there are also a few cement producing countries which do not have enough cement-grade limestone resources, and accordingly international trade has increased, especially in the high-end, value-added product range. Countries with no sufficient limestone resources include Bangladesh, Cameroon and Kuwait, to mention a few.

Imports and exports

The traded quantity of limestone which is used for the cement and lime production was about 60 Mt/a in 2019. The trading value was about US$ 950 million. In the Top5 list of limestone importers were India (46.4% of global imports), Bangladesh (6.5%); Taiwan (5.0%), South Korea (4.2%) and Kuwait (3.7%). The Top5 Exporters were UAE (40.3%), Vietnam (8.4%), Oman (7.6%), Japan (7.5%) and Malaysia (5.9%) [3]. Figure 5 demonstrates how limestone imports have increased in India over the last few years. From FY 2010-11 to 2019-20 imports increased more than 5-fold, while at the same time cement production less than doubled. There are several reasons for this. Possible reasons are the limestone resources in India and their distribution, the limestone grades and eventually the state-wise auctioning procedures of limestone blocks by the Indian Mines Department.

Limestone resources in India

In the latest limestone resource assessment by the Indian Bureau of Mines (IBM) in 2015, the total reserves were stated to be 203 billion t. Karnataka is the leading state holding 27% of the total limestone resources, followed by Andhra Pradesh and Rajasthan (12% each), Gujarat (10%) and Meghalaya (9%) [4]. The total reserve, which is the economically mineable part of the measured resources was classified as 16.3 billion t, of which 9.4 billion t (58%) is the proven reserve and 8.6 billion t the proven cement grade reserve (Figure 6). Based on the expected growth and consumption pattern, which forecasts a requirement of about 600 Mt/a of limestone by the cement industry in 2030, the proven cement grade will only last for another 15 years, unless the reserves can be fundamentally improved by introducing more economical mining methods. Accordingly, several cement producers in India are working on the subject by implementing advanced measures such as geochemical assessment and online X-ray diffraction (XRD) analysis for material characterization.

Limestone grades

In India, according to cement industry sources, most of the limestone deposits which are available for the cement industry are of marginal grade, below the cement grade, which has an acceptable range of 44 to 52% CaO content, providing oxides to satisfy LSF, silica and alumina modulus and limiting MgO content to (max) 3.5% for the production of OPC (Ordinary Portland Cement). Many of the deposits that have come up or are likely to come up for auction have high silica and low to sub-grade CaO content and many of the deposits also have a high MgO content. This type of deposit cannot be utilized for the cement manufacturing process without blending with high grade limestone. However, due to better process control of the limiting value of MgO, usage can be enhanced from the present 3.5% to 5% (max). Furthermore, deposits with high SO3 content restrict the usage of petcoke as fuel, which restricts the use of low grade limestone.

In Figure 7 the S.-Korean and Vietnamese limestone reserves are compared. In S.-Korea, high-grade reserves with a CaO content above 52% account for 12% of the total reserves, while in Vietnam it is only 8.5%. However, in absolute quantities, Vietnam’s reserves of high-grade limestone are more than 5 times larger than those of S.-Korea [5]. In Vietnam, there are 4 main regions with high-grade reserves: Northeastern limestone, Northwestern limestone, Northern-Central limestone and Southern limestone. In total, there are 351 limestone deposits in Vietnam, of which 274 have been investigated. However, most of the clinker manufacturing plants are located in the north, while cement markets are primarily in the south. This is the main reason that in Vietnam there are many split grinding plants and that clinker has to transported from the north to the south.

Limestone quality deterioration

In India, there are many limestone deposits where the quality is deteriorating for several reasons. The largest Indian cement producer UltraTech Cement, which is part of the Aditya Birla Group, has just this year been awarded a five-star rating for sustainable mine management for 10 of its limestone mines by the Ministry of Mines and Indian Bureau of Mines. One of them is the Kovaya limestone mine, which supplies the Gurajat cement works (Figure 8). The Kovaya limestone mine is a marginal grade limestone deposit, intermixed with marl. The quality of the limestone and marl varies from 31% to 46% CaO. The limestone quality deteriorates with depth and the remaining limestone varies between 40% and 42% CaO. For manufacturing OPC cement, UltraTech is now in the position to accept this material, when blending it with high-grade limestone.

Holcim’s Nobsa cement plant close to Bogota Colombia (Figure 9), is sourcing limestone from 3 quarries, including their own self-operated Nobsa quarry. The Nobsa limestone deposit is a complex geological body. The area consists of very different layers, and the vertical nature of the interbedded limestone, marl and clay make exploration drilling complicated, especially after several years of exploitation and a deterioration in the limestone quality. The quarry lacked a high quality geological model, which made it difficult to understand and therefore to manage the variability in the quality of the material. Now, Holcim is using advanced industry-leading 3D modelling to rapidly integrate, communicate, and interpret geological data of the deposit. With the new model it became possible to extract most of the limited high-grade layers and to maximize the use of low-grade material, which was previously wasted.

3 Cement production

3.1 Market trends

Figure 10 shows the cement production outlook up to 2030. According to this projection production is to increase from 4097 Mt/a in 2017 to 4333 Mt/a in 2021. In this period China’s share is almost constant at around 56% of the global cement production. However, as from 2021 China’s cement production will decline and so will China’s share on the global market. Accordingly, global cement production will decline to 4081 Mt/a by 2030 with China’s share at 41.7%. The Rest of the World (RoW) will significantly increase its cement production from 1970 Mt/a in 2021 to 2381 Mt/a by 2030. Figure 11 illustrates the clinker quantities that will be produced as well as the required cement additives to produce the before mentioned cement quantities. So finally, with a projected clinker factor of 0.68 there will be 1306 Mt/a of cement additives necessary by 2030, a quantity larger than ever before. 3.2 Example Germany

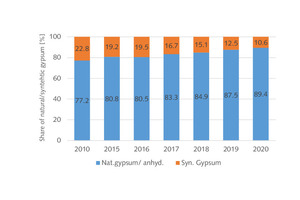

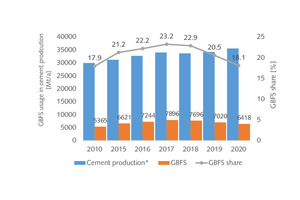

Germany is using roughly 5.15% of gypsum in its cement production. Figure 12 shows how the share of used natural gypsum and anhydrite related to the use of FGD-gypsum has developed over the years. In all the years since 2010 the share of FGD-gypsum has declined. In 2020 only 10.6% was synthetic gypsum, which shows a decline by more than 50% since 2010. The situation for GBFS in Germany is also alarming but not as bad as the situation with FGD-gypsum., Figure 13 shows the GBFS usage in Germany up to 2020. There is also a massive decline in the GBFS quantities used since 2017, however the GBFS share in 2020 was still at the level of 2010. But all in all, it can be stated that in Germany there are already significant supply problems with FGD-gypsum and granulated blast furnace slag.

3.3 Availability of GBFS

OneStone Consulting has just finished a new market study about the future of granulated blast furnace slag (GBFS) [6]. The report provides figures for the production, trade and consumption of GBFS for 110 countries, derived from the pig iron production in those countries and international trade figures. Depending on the development of the iron & steel industry, an outlook is given for 2025 and 2030. There are some industry sources which suggest that already in a few years the elimination of blast furnaces will cause the availability of GBFS to significantly decline globally. However, the truth is that the restructuring of the steel industry will come in cycles starting in W.-Europe and other developed regions before it is implemented in developing countries. As a result, BF/BOF steelmaking, which relies on iron ore, will continue to be the dominant processing route for the manufacture of steel.

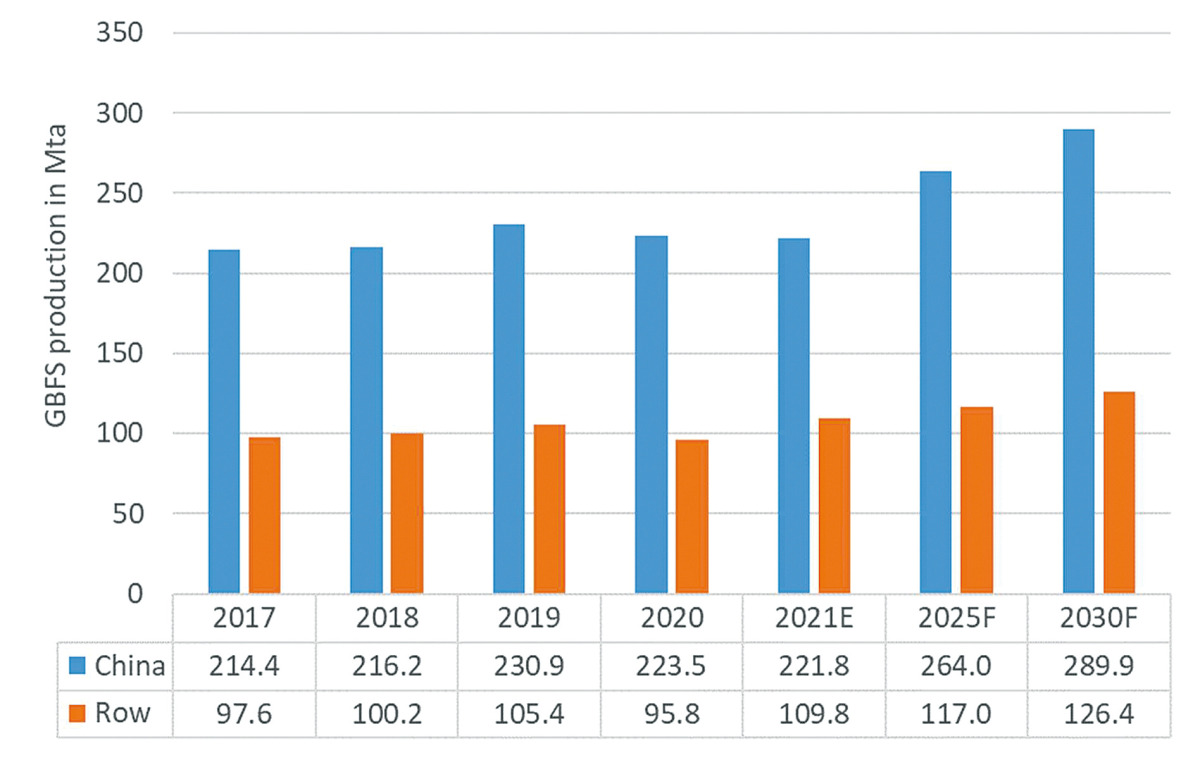

The global pig iron production is projected to increase from 1350 Mt/a in 2021 to 1384 Mt/a in 2025 and 1403 Mt/a by 2030. Due to a higher pig iron production and increasing slag rates, global blast furnace slag (BFS) production will increase from 382.7 Mt/a in 2021 to 418.5 Mt/a in 2025 and 445.4 Mt/a by 2030. Another effect is that the granulation rate for BFS will increase from today’s 86.6% (worldwide) to 93.4% by 2030.This will increase the global GBFS production from 331.3 Mt/a in 2021 to 381.1 Mt/a in 2025 and 416.6 Mt/a by 2030 (Figure 14). Many world regions will become GFBS exporters. Accordingly, there should be enough GBFS available for imports and to substitute fly ash in cement and concrete, also in the EU 27, where GBFS production will decline by almost 30%.

3.4 Availability of fly ash

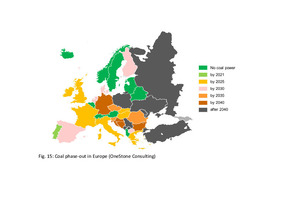

The availability of fly ash depends heavily on the outlook for hard coal fired power. In Europe, the coal phase-out has a high political and social priority. Figure 15 shows the timetable of the various governments to phase coal out in Europe. Accordingly, the European power plant industry will already be coal-free in 2040, with the exception of Poland. Europe is thus playing a pioneering role on a global scale with a large effect on the future availability of fly ash. However, due to the energy crisis with increasing prices for natural gas, the coal demand for power plants significantly increased in 2021, after a decline in 2020. According to the latest BP Statistical Review of World Energy, in Europe coal-fired electricity generation increased in 2021 to 632.0 terawatt-hours, which is an increase by 10.9% compared to 2020. This was even higher than the global increase in coal-fired power electricity generation which was only 8.5%.

On the global scale, the amount of new coal-fired power plant capacity still exceeds retirements. According to the Global Coal Plant Tracker, July 2022 [7], 312.8 GW of new coal-fired power plant capacity was installed worldwide from 2017 to 1H of 2022 (Figure 16). Of this, 74.1% was in China and India alone and 25.9% in the Rest of the World. In the same period, only 188.5 GW of existing coal-fired power plant capacity was retired or decommissioned (Figure 17). China and India account for 21.9% of this capacity, with the Rest of the World accounting for 78.1%. Accordingly, China and India increased their coal-fired power generation capacity by 190.6 GW on a gross-net basis in the period from 2017 to 1H 2022, and the rest of the world decreased capacity by 66.3 GW. Today, another 172 GW capacity of coal-fired power is still under construction, with most of it in China, India and SE Asia.

3.5 Availability of FGD-gypsum

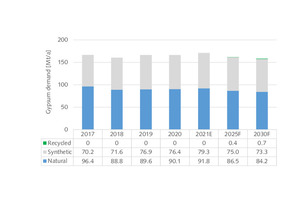

In 2019, the global cement industry used 166.5 Mt/a of gypsum as a cement retarder. Of this amount 89.6 Mt/a (53.8%) was natural gypsum (incl. anhydrite) and 76.6 Mt/a (46.2%) was synthetic gypsum, while recycled gypsum in the cement industry is still close to zero (Figure 18). China alone was responsible for 72.1% of the synthetic gypsum, which beside FGD-gypsum also comprises a growing amount of phosphorus gypsum. Figure 19 is a projection of the gypsum demand by the cement industry up to 2030. It has to be noted that the gypsum rate in cement has already been in decline since 2017, when the global gypsum rate in cement was 4.07%. In 2019, the rate declined to 3.97% because of an increasing production of blended cements. For 2030, a gypsum rate of 3.88% is projected. Despite the lower global gypsum demand in 2030, synthetic gypsum will have an almost unchanged market share and natural gypsum will lose market shares against recycled gypsum.

5 Outlook

The adequate supply of raw materials for the cement industry has become an issue. This is also the case for limestone, which is by far the most used raw material, being extracted from quarries almost in the same quantity as coal. For example, the cement-grade limestone reserves in India might come to an end sooner than expected putting the expansion of the cement industry in danger. For 50-year lease contracts the Indian Bureau of Mines lately achieved record revenues. In countries such as Switzerland the future cement production is also in question. Due to public resistance to raw material quarry expansion projects and local Swiss law, some projects are on hold. Without new permits for quarry expansions the Swiss cement production could fall to around 64% in a few years. If all expansion projects are approved by 2023, the decline in Swiss cement production will be delayed until the end of 2030.

The future of cement additives such as GBFS, fly ash and FGD-gypsum will depend mostly on political decisions and the development of the power plant industry and iron & steel industry. Coal-fired power plants and blast furnaces have a future if carbon capture, utilization and storage (CCUS) projects are implemented [8]. Now studies exist that show that for China and many other countries there are huge possibilities for CCUS technologies to support the transition to green technologies. The power plant industry might try to make the transition without CCUS by investing in renewable energy. The iron & steel industry has not so many options and there are industry sources which already came to the conclusion that blast furnace + CCUS is the only technology that can be adopted with speed and scale, while large scale green hydrogen adoption is unlikely before 2040.