Establishing carbon-negative cement factories – a roadmap for Germany

Energy Post [5]

Energy Post [5]

Scientific World Journal [7]

Scientific World Journal [7]

NeoCarbon [8]

NeoCarbon [8]

NeoCarbon [8]

NeoCarbon [8]

Langfristszenarien [13]

Langfristszenarien [13]

Lawrence Livermore National Laboratory [14]

Lawrence Livermore National Laboratory [14]

Oxford Institute for Energy Studies [16]

Oxford Institute for Energy Studies [16]

Ener Data [17]

Ener Data [17]

Regulatory pressures from the EU and Germany, coupled with increased public scrutiny of cement companies’

environmental impact, have prompted several firms to commit to the Net Zero target by 2050.

To reshape the public image of the cement sector, from being a heavy polluter to pioneer of innovative

sustainability practices, and ensure cement business’s viability, we propose establishing Germany’s

first carbon-negative cement plant, employing a blend of point source capture and direct air capture (DAC) technologies. This revolutionary solution not only addresses existing challenges faced by cement producers but also offers cement companies resilience against CO2 pricing impacts. In this article, we aim to outline the challenges confronting cement manufacturers and demonstrate how a combination of point-source capture from the flue gas and DAC can alleviate them. Additionally, we will provide insights into suitable DAC technology who can seamlessly integrate into our proposed solution.

1 Climate Goals

CO2 neutrality via carbon removal technology

The European Union (EU) is committed to achieving economy-wide climate neutrality by 2050 and aims to reduce emissions by at least 55% by 2030. By 2040, around 280 million t of CO2 must be captured to meet this objective, with the EU targeting approximately 450 million t of CO2 capture by 2050 [1].

Germany has set even more ambitious goals, aiming for climate neutrality by 2045 and carbon negativity thereafter. To achieve this, emissions must be reduced by 65% by 2030 and at least 88% by 2040 compared to 1990 levels. Carbon removal measures are essential in tandem with emission reduction efforts. CCS technology is typically categorized as a reduction technology, whereas DAC technology is recognized as a carbon removal technology. And the combination of the two can optimize benefits. For example, the BMWK (German Federal Ministry for Economic Affairs and Climate Action) document underscores the significance of carbon removal while recognizing the potential of achieving carbon negativity by combining DAC technology and CCS [2]. Furthermore, both technologies are endorsed by the EU’s Net-Zero Industry Act, which aims to bolster the application of net-zero technologies to fulfill 40% of the EU’s annual deployment requirements by 2030 [3].

Cement industry bears crucial responsibility for Germany’s ambitious climate targets

Net zero technologies are essential, especially for certain sectors with high emission intensity and energy intensity such as steel, cement production, and chemicals. Those sectors are logically also the focuses of Germany’s decarbonization plan [4].

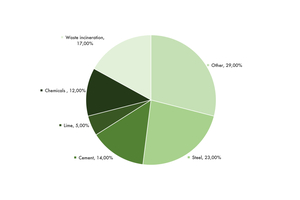

In 2021, the cement industry in Germany alone accounted for 20.1 Mt of CO2 emissions, ranking just behind the steel industry and waste incineration, which emitted 31.5 Mt and 23.3 Mt respectively, according to data from the EU Emission Trading System. When considering both the cement and lime industries together — as the lime industry is overwhelmingly linked to cement production — they are ranked as the second-largest emitters within the industrial sector, contributing to 19% of the total emissions.

Given its status as one of the largest emitters, individual companies in the cement industry within Germany wield considerable impact potential over the nation‘s ability to reach its climate targets. It is important to transform the German cement industry to be both competitive and climate-friendly.

2 Cement & CO2

CCS and Carbon Removal bundle solution

can rebuild the industry’s public image

Besides the challenge of decarbonizing its operations for cement business, an equally challenging task for cement players is to change their public images. In a recent report published by WWF Germany, the 30 largest emitters in Germany were identified and phrased as the ”dirty thirty“ — a name easy to remember for readers but difficult for emitters to bear. Regrettably, cement producers are logically also among the entities categorized as the largest emitters in this report [6].

However, through our diligent study, we believe that establishing Germany’s first-of-a-kind carbon-negative cement plant, utilizing a combination of CCS and Carbon Removal technologies, offers a solution to shift the industry’s reputation positively. Our DAC technology distinguishes itself from other carbon removal methods by leveraging existing infrastructure like cement plants compared to doing large and costly greenfield operations.

Cement production typically generates significant quantities of CO2 emissions during its calcination process. The process that produces the most CO2 is the calcination of limestone (calcium carbonate) to produce clinker. During this process, limestone (CaCO3) is heated in a kiln to temperatures above 900°C, which causes it to decompose into calcium oxide (CaO) and carbon dioxide (CO2). This chemical reaction releases significant amounts of CO2 into the atmosphere.

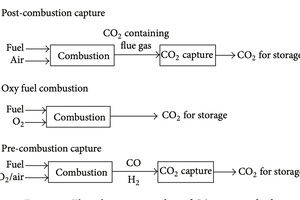

Various methods exist for capturing carbon from cement production, encompassing post-combustion, oxy fuel combustion and pre-combustion techniques (Figure 2) [7]. Those initiatives largely focus on capturing emissions at the source of CO2, before it would otherwise be released into the atmosphere via the exhaust system (e.g. fume stacks or chimneys). Such approaches are thus named Point-Source Capture (PSC). Depending exclusively on PSC prevents a factory from attaining Net-Zero status, let alone achieving carbon negativity. Indeed, PSC can typically capture only up to 90 to 95% of the emissions of CO2, leaving still millions of t/a of CO2 to be released into the atmosphere in Germany alone.

Additionally, it is also acknowledged that only carbon removal technologies have the capacity to remove the most challenging hard-to-abate carbon emissions, amongst which Direct Air Capture (DAC) — or capturing CO2 directly from ambient air — has the strongest potential for immediate, scalable and directly measurable CO2 removal [8].

Yet, it’s essential to acknowledge that every technology has its own set of advantages and disadvantages. The optimal approach often involves integrating multiple technologies to achieve the most favorable outcomes. The optimal solution we can envision is the designated PSC + DAC bundle solution.

On one hand, by combining PSC and DAC technology, carbon emissions are reduced and CO2 is removed simultaneously, resulting in a net-negative industry. In fact, PSC excels in efficiently capturing carbon emissions from exhaust gases. However, it falls short in achieving net-zero emissions or carbon negativity, as it cannot capture the entirety of the source’s emissions and lacks the capability to remove CO2 already present in the atmosphere. In contrast, DAC technology specializes in capturing carbon from ambient air, and thus achieving net-negativity. DAC’s engineering-driven methodology, coupled with its ability to operate at extremely low CO2 concentration levels, renders it deployable across diverse environments.

On the other hand, such a combination would alleviate DAC’s primary drawback: its substantial energy requirement. Typically, a DAC system demands a significant amount of energy to capture CO2 from ambient air, where CO2 concentration is merely 0.04%. Relying solely on renewable energy sources to power these machines is currently cost-ineffective and results in lower net carbon removal efficiency. Fortunately, within the bundled solution, industrial sites eligible for PSC often generate substantial amounts of “waste heat” as a byproduct of their processes, which serves no practical purpose for the factory. Typically, this heat is released into the atmosphere without further utilization, thus being wasted. However, within the bundled solution, DAC machines can use this waste heat as an energy source for the carbon capture process. Utilizing this heat for DAC processing would enable highly cost-efficient removal, accounting for 15–25% of the factory’s emissions — ultimately leading to the PSC + DAC bundled solution removing over 100% of the emissions, or in other words, a carbon-negative factory.

2.1 Calculation Example

Under the PSC + DAC bundle solution, a DAC company like NeoCarbon will collaborate with its PSC partner to establish a strategic alliance. Both DAC and PSC will deploy their respective technologies at industrial sites belonging to cement companies. While the PSC company focuses on capturing CO2 from exhaust gases, the DAC company will utilize the waste heat generated in the process to capture CO2 from ambient air.

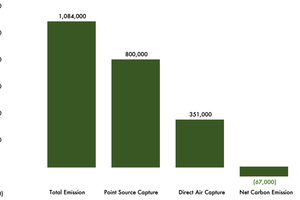

This approach has been theoretically validated using an existing industrial site emitting over 1.08 Mt/a. By installing PSC technology, it is possible to economically capture up to 74%, totalling a maximum of 800000 to/a. However, by also leveraging the site’s waste heat, currently unused, NeoCarbon’s technology can capture an additional 32%, or 351000 t/a. In total, this results in capturing 1151000 t/a while emitting 1084000 t, effectively transforming the entire factory into a carbon sink.

As of the report date and our current knowledge, this collaborative effort in carbon capture represents the world’s inaugural project combining point-source and DAC technologies with the goal to achieve the first carbon negative factory. A recent study by Edwards et al. estimated that DAC could reach up to 4.9 Gt CO2 removal by mid-century, depending on public acceptance, regulatory support, and deployment rates [9]. However, the study does not give any indication of the concrete potential of the DAC for the cement industry. Therefore, we will use the knowledge gained from the theoretical validation to assess the removal potential of DAC for European and global cement production.

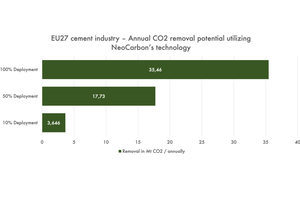

Each ton of cement produced emits on average 0.6 t of CO2 [10]. In 2022, the EU27 produced 182.5 Mt of cement, corresponding to 108 Mt of CO2. Based on the available waste heat of previously discussed plants, we know that for every 1084 kt of CO2 emitted, NeoCarbon can remove 351 kt of CO2 using the waste heat of the cement plant. Extending this calculation to all cement production sites in the EU27, we can potentially remove 35.46 Mt/a of CO2.

The same calculation allows us to estimate the global potential of NeoCarbon’s waste heat recovery technology. In 2022, the global cement production was 3359 Mt. With NeoCarbon‘s DAC retrofit approach, a total removal potential of 652.59 Mt of CO2 per year becomes feasible.

These scenarios are only a rough calculation and additional important factors have not been considered, but they allow us to estimate the huge potential of DAC for a successful energy transition. Importantly, DAC is particularly compatible with other sustainability approaches, as the retrofit method allows for seamless potential integration into more than 100 cement plants already operating in the EU.

3 PSC & DAC Approach: A Path for Effective

Implementation

NeoCarbon GmbH, based in Berlin, is a DAC company which is offering solutions for carbon-negative factories. It is supported by prominent investors including RAISE Ventures, PropTech1 Ventures, SpeedInvest, and Antler, renowned for their investments in the DeepTech sector.

Leveraging waste heat and existing infrastructures, NeoCarbon captures carbon at a high scale. By utilizing industrial sites, NeoCarbon drastically reduces costs and accelerates the deployment of DAC technology. Based on today’s availability of low-grade industrial waste heat globally, NeoCarbon already has the potential to capture over 1.3 gigatons of CO2 annually, thereby also enabling the transformation of cement factories into carbon-negative facilities. NeoCarbon’s utilization of waste heat alongside a retrofitting strategy establishes its qualification as a DAC partner. Moreover, its innovative reactor design is essential for unlocking further scaling to capture even more CO2 from ambient air.

3.1 Leveraging waste heat

DAC is known for its energy intensity and reliance on abundant renewable energy sources. NeoCarbon has innovatively embraced a technology that uses waste heat to largely power their systems. NeoCarbon’s process efficiently utilizes waste heat at low temperatures starting from 30 °C. The higher the temperature of the waste heat, the less electrical energy is required to power NeoCarbon’s installations, resulting in enhanced efficiency. Considering that cement plants typically generate waste heat at higher temperatures at 110-130 °C, NeoCarbon’s approach undoubtedly offers an energy-efficient and technically compatible solution.

3.2 Retrofitting approach

As NeoCarbon leverages waste heat, it operates on sites with a high amount of such otherwise unusable heat. These can systematically be found at cement plants. A major concern for many waste heat generators revolves around the technical compatibility of their industrial sites with the waste heat users’ technologies [12]. Achieving technical alignment may necessitate additional investments in research, testing, and dedicated manpower and time commitments. Consequently, this poses a significant barrier for many companies considering putting their waste heat in use.

Fortunately, NeoCarbon offers a solution to circumvent these daunting obstacles. Through a transparent retrofitting approach, NeoCarbon can seamlessly install its DAC machines into existing industrial sites without the need for additional greenfield construction, and without interrupting or impacting the production processes of cement plants. This approach minimizes technical hurdles, eliminating the need for substantial investments in finding compatible solutions or integrating new technologies into existing or new plants.

3.3 Novel reactor design

NeoCarbon’s monolithic reactor design further sets it apart from other Direct Air Capture companies. This reactor has several clear advantages. Firstly, it leads to better heat management: the heating and cooling liquid can be distributed more precisely, leading to faster cycles and a lower heat requirement. Secondly, it limits sorbent degradation over time. The precision with which the heat can be delivered via the reactor makes it possible to control the partial pressure locally, thus improving the desorption step. Lastly, the design is modular and therefore easily scalable as the reactors can be stacked.

4 Upcoming Benefits

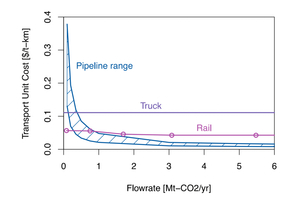

The upcoming CO2 pipeline project in Germany further fuels the unprecedented PSC + DAC bundle solution. In addition to the amplified benefits offered by the bundled solution, which combines PSC’s pricing advantages with NeoCarbon’s unique DAC approach, another key advantage of this strategy lies in its alignment with Germany‘s CO2 pipeline project.

By connecting cement production plants to CO2 pipelines, it unlocks additional potential within the bundled solution. This facilitates more convenient and cost-effective transportation of CO2, leveraging the infrastructure to store CO2 securely and permanently. This approach presents a superior cost-effective alternative to traditional methods such as transportation trucks or trains to other sequestration sites. Indeed, NeoCarbon’s captured CO2 can thus benefit from the economies of scale normally only reachable with PSC technologies, yielding a cost-per-ton for transport well below what an efficient large standalone DAC site would manage. Similarly, liquefaction of the removed CO2 via DAC, another significant cost for traditional DAC solutions, also benefits from the much larger scale of PSC liquefaction solutions ahead of the transport via pipeline.

In light of the aforementioned reasons, the Federal Government acknowledges the essential role of CO2 infrastructure and plans to amend the legal framework to facilitate the deployment of CO2 pipelines. For instance, in order to initiate the construction of privately operated CO2 pipelines within a state regulatory framework, amendments to the Carbon Storage Act will be promptly enacted in accordance with the Federal Government’s proposals outlined in the report from the end of 2022. The areas of legal uncertainty in the application of the act will be remedied [15].

In the forthcoming decades, the advantages of innovative technology solutions will become increasingly evident. Investing in and constructing a plant entails making long-term decisions that will profoundly shape the industry‘s trajectory in the decades to come. Therefore, it is imperative that plant/factory decisions align with anticipated market and technology landscapes in the forthcoming years.

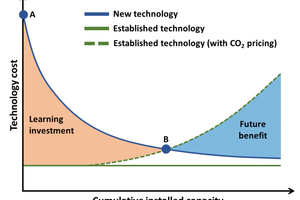

We can use the CCS technology as an illustrative example to demonstrate how the trajectory of CO2 prices will affect the future benefits of cement plants. While the current costs of conventional technologies appear low, companies will face mounting costs in the future. A recent study from the Oxford Institute for Energy Studies illustrates this through two curves: the blue curve representing the learning curve of the new technology (e.g. cement production with CCS), and the green curve depicting the cost of established technology (e.g. cement production without CCS).

Initially, the new technology incurs higher costs (point A), such as when a First-Of-A-Kind (FOAK) plant is deployed. Conversely, the established technology’s costs are notably lower. However, the incremental rise in environmental costs, such as higher CO2 prices, leads to the formation of a dotted green curve, leading to a moment where the new technology becomes more beneficial (point B). This graph delineates two distinct areas: the learning investment and the future benefit. As the cumulative installed capacity of the new technology grows, its cost reduces. Notably, higher CO2 prices occurring earlier in this progression would yield lower investments and greater benefits.

Moreover, transformation to carbon-negative factories mitigates potential risks associated with emission rights. In fact, CO2 prices have already begun to impact the economics of established cement plants. With ETS emission rights priced at over 70 € for the next foreseeable five years and with potential for further increasing beyond 2030, the issue of CO2 emissions presents a significant challenge for these plants.

On one hand, cement plants with high emissions face additional financial strains, which could impede their capacity to operate at full capacity. The cost of obtaining extra permits to offset increased production emissions counterbalances any potential gains, resulting in a decline in operational capacity that poses a threat to their economic sustainability. In stark contrast, carbon-negative factories remain unaffected by these concerns. Upfront investments in technology integration yield long-term benefits, optimizing production efficiency and shielding them from the financial impacts of CO2 pricing.

On the other hand, cement plants also encounter challenges in autonomously adjusting their product development and production processes to align with market demand. CO2 emissions and associated costs have emerged as influential factors shaping their product development and R&D strategies.

Market demand plays a pivotal role in the cement business. For instance, an analysis of CO2 emissions in the European cement sector by Umweltbundesamt revealed an intriguing trend during the second and third trading periods of the EU Emissions Trading Scheme (ETS): the clinker share increased alongside CO2 emissions since the scheme’s inception when generous allowances were still granted to companies. One plausible explanation is the growing demand for higher-quality products with a greater clinker share. However, with the significant rise in the price of CO2 emission rights since the scheme’s inception, conflicts have arisen between CO2 prices and the freedom of choice in product development and R&D strategy. Resolving these sometimes inevitable conflicts between market-oriented decisions and environmental sustainability responsibility necessitates innovative solutions [18].

Fortunately, the DAC + PSC solution can solve this challenging task. By establishing carbon-negative factories, cement manufacturers can mitigate the impact of fluctuating ETS prices on their product development and research processes while contributing to the overarching carbon-neutral objectives of the EU and Germany. As carbon emissions are negative, the price of emission rights has no additional impact on these processes.

5 Conclusion

As Germany aims for climate neutrality by 2045, the cement sector stands as responsible for a significant share of carbon emissions. Regulatory pressures and public scrutiny necessitate innovative approaches to mitigate environmental impact while sustaining industrial growth. This paper outlines an innovative strategy: leveraging the synergies between Point-Source Capture (PSC) and Direct Air Capture (DAC) to pioneer carbon-negative cement production.

Our proposed solution entails the seamless integration of PSC and DAC technologies within cement manufacturing processes. PSC targets emissions from exhaust gases, preventing a portion of it from being released into the atmosphere. Simultaneously, DAC removes CO2 directly from ambient air, offering a comprehensive approach. Specifically with NeoCarbon’s waste heat based approach and its seamless retrofitting of industrial sites, the synergies lead to remarkable potential. By combining the two, it is not only possible to achieve emission reduction but also to strive toward carbon negativity — a landmark achievement in sustainable industrial practices.