Market trends for green cements

Pexels, Joao Jesus

Pexels, Joao Jesus

Global Forest Watch

Global Forest Watch

Oyak Cement

Oyak Cement

Cembureau

Cembureau

IEA

IEA

IEA

IEA

Aalborg Cement

Aalborg Cement

DTI

DTI

DTI, Torben Eskerod

DTI, Torben Eskerod

![9 ACT production processes [6]](/uploads/images/2023/w300_h200_x600_y379_Fig9L_ACT1-7ad9fce3f4f49e36.jpeg)

![10 CO2 contribution of ACT processes [6]](/uploads/images/2023/w300_h200_x600_y307_Fig10L_ACT2-c58a117fcc228ef7.jpeg)

Schwenk Zement

Schwenk Zement

K. Scrivener, EPFL

K. Scrivener, EPFL

Cementos Argos

Cementos Argos

Hoffmann Green Cement

Hoffmann Green Cement

Cimpor Global Holdings

Cimpor Global Holdings

Green cements are booming, because of the net-zero journey of the cement industry to become carbon-neutral by 2050. But what contribution can green cements provide to reduce CO2 emissions in the cement industry? What are the latest market trends for green cements and which types of green cement will have a major impact? In this article a number of answers will be given.

1 Introduction

Buildings account for an estimated 37% of the global CO2 emissions. About 1/3 is generated during the construction phase, while 2/3 are generated during the lifetime of the buildings and the corresponding energy consumption. For the construction the use of concrete and mortars, which are both made by using cement, is irreplaceable. If 25% of cementitious products were replaced by timber, this would require the planting and harvesting of a forest 1.5 times the size of India. But in real terms, because of deforestation and fires, forest loss has become a problem on all continents (Figure 1). So, what other solutions will work if there are no alternatives to cement and concrete? The answer is low carbon cements or “green cements”. Alfacem (Figure 2), EcoCem, EcoPlanet, Ekkomaxx, FutureCem, Geopolymer cement and LC3 are some examples of green cements. However, some of them are only a new name for cement or concrete additives, which were previously known as fly ash and slag cements or concrete additives.

2 Green cement challenges

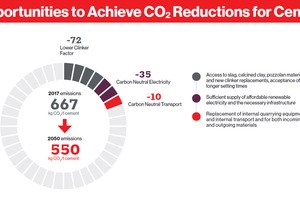

Green cements are booming, because of the net-zero journey of the cement industry to become carbon-neutral by 2050. Figure 3 shows what green cements can contribute to the net-zero journey. The figures have been provided by CEMBUREAU, the European Cement Association. According to these figures, by further reducing the clinker factor another 72 kg/CO2 can be avoided, which is about 10.8% of the 667 kg CO2/t cement emissions, based on the output in 2017 [1]. So we are only speaking about 10 to 11% of future CO2 reductions. In 2017, the clinker to cement ratio (clinker factor) in Europe was 77%. With new ambition, CEMBUREAU is aiming to move from that level to 74% by 2030 and 65% by 2050. This shall be achieved by new cement types as well as traditional clinker substitutes such as fly ash and granulated blast furnace slag and non-traditional clinker substitutes such as calcined clay.

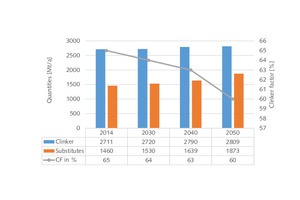

To calculate the future amount of green cements and clinker substitutes, a projection by the IEA [2] dating from the year 2018 is often used. Figure 4 shows the global average composition estimates for cement in 2014 and 2050. According to the IEA, the clinker factor will decrease from 65% to 60%, while granulated slag and fly ash will significantly decrease and limestone and calcined clay will increase. It really gets interesting when the cement production levels predicted by the IEA are taken into account (Figure 5). According to the IEA projection, the global cement production will grow steadily from 4171 million annual t (Mt/a) in 2014 to 4682 Mt/a by 2050. With a clinker factor of 60% by 2050, about 1873 Mt/a will be non-clinker components in cement, with about 375 Mt/a made up by calcined clay alone. However, many of these data are questionable, for example the amount of granulated blast furnace slag (GBFS) and other metallurgical slags in the cement composition.

Another challenge is the declining availability of GBFS, fly ash and other natural pozzolans. According to a OneStone report [3], the production of GBFS in Europe will decline from 24.7 Mt/a in 2021 to 21.5 Mt/a by 2030, which is a decline by 13%. In Western Europe alone, the GBFS trade balance will become negative and to fulfil the needs of the cement and concrete industries, about 6.5 Mt/a of GBFS will have to be imported in 2030. In other regions, especially in Asia, the production of GBFS will significantly increase up until 2030. According to our projection, the global GBFS production will increase from 331.3 Mt/a in 2021 to 381.0 Mt/a in 2025 and 416.6 Mt/a by 2030. China will have the largest growth, while in the RoW the GBFS production will also grow, due to increasing slag rates and additional BFS granulation plants. At the moment it’s very difficult to project the situation up to 2050, but the IEA projection assumption of only 1% GFBS in the cement mix 2DC and the transition of the steel industry to carbon neutrality is more than questionable from today’s viewpoint.

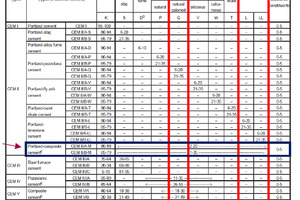

The next challenge is the adaption of cement standards. Let us just take the example of calcined clays and LC3 cements and the European cement standards into account. Limestone-calcined clay cement is allowed in the European cement standard EN 197-1 as CEM II/A-M and CEM II/B-M (Figure 6). However, the minimum clinker content has to be 65% and limestone + calcined clay can only be in a range of 12-35%. LC3 cements have been proven to have a similar quality to Standard Portland Cement, but they are composed of 50% clinker, 35% calcined clay, 15% limestone and 5% gypsum. Accordingly, the full potential in CO2 reduction is not possible with the EN 197-1. The hope of the industry is the new EN 197-5, which is especially for ternary cements, where new types of CEM II/C-M and CEM VI are allowed. But it has to be noted that in EN 197-1, CEM III/C cements already allow a clinker content of only 5-19%, while 81-95% GBFS are allowed.

The new EN 197-5 standard is the result of many years of research focusing specifically on the durability of low-clinker concretes (Figure 7 and Figure 8) [4]. The idea behind it is to grind the clinker component finer and combine it with a cementitious component and limestone. Compared to CEM I Portland cement with 95 % clinker content, the CEM II/C-M and CEM VI cements covered by EN 197-5 will enable the wider use of low clinker cements towards the goal of CO2 neutrality in concrete construction. For CEM II/C-M Portland composite cements, the clinker content can be reduced down to 50 % by mass and for composite cements in the CEM VI group down to 35 % by mass. The EN 197-5:2021 has already been implemented by a number of European countries. But there are also countries which will need more time for the adaptation.

3 Green cement developments

Over the years, many new cements and alternative clinker technologies (ACT) have been developed [5, 6], but still at this time it is difficult to say which ACTs will have the largest impact as an alternative to OPC clinker. The main options under review are: Belite-rich clinker, CSA clinker, BYF clinker, X clinker and Celitecement. Reactive belite cement contains the same 4 cementitious phases (alite, belite tricalcium aluminate, and tetracalcium aluminoferrite) as Portland cement, but in different proportions. With lower sintering temperatures of 1250 °C instead of 1450 °C, more belite and lower alite phases are produced and accordingly the CO2 formation is reduced. CSA (Calcium sulfoaluminate) clinker also uses temperatures of 1250 °C. CSA cements were developed in the 1970s to compensate the lower early-age strengths observed in belite-rich cements. Typical raw materials used in the production of CSACs are limestone, calcium sulfate and aluminum-rich minerals or industrial by-products.

BYF (Belite-ye’elimite-ferrite) clinker can also be produced at temperatures of 1250 °C but at lower costs than CSA clinker, because the relatively expensive aluminium-rich raw materials can be reduced, resulting in a higher proportion of silicate and ferrite phases. X-clinker is a development by Cimpor and Tecnico in Portugal. The production process allows the use of traditional raw materials, such as limestone, clay, marl and sand by melting the raw mixture at a temperature of 1550°C. However, because much less limestone is used, the CO2 balance of the process is 25% lower than the one for standard clinker. Celitement goes a completely different way. The technology, which has been acquired by Schwenk Zement in Germany, in principle uses CaO, SiO2 and water as raw materials. The production process is made up of two main process steps by using an autoclave to produce a non-reactive CSH intermediate product and a special grinding step to transform the autoclaved intermediate into the final reactive product.

Figure 9 shows a simplified schematic representation of the stages considered within the production processes of the ACTs under review [6]. The comparison also includes the standard OPC production process for reference purposes and the Solidia cement approach. Solidia is a non-hydraulic binder produced using the same raw materials as OPC, but with a lower amount of CaCO3 and a kiln temperature of around 1200°C. According to the figure, Solidia has an overall C/S molar ratio of around 1, but it needs to be cured by exposing the concrete mixture to a high-concentration gaseous CO2 environment of 60 to 90%. Anyhow, it has to be noted that only the Celitement and the X-Clinker presently consider a scenario of full process electrification, while the other solutions follow a fuel combustion-based concept, similar to the existing clinker production processes.

Figure 10 indicates the CO2 contributions for the energy- and material-related emissions of the various ACTs reviewed [6]. Because the X-clinker and Celitement production processes can be fully electrified, depending on the nature of the electricity used, the thermal component of CO2 emissions of these processes could be completely eliminated, which will give them a huge benefit in comparison to the other processes when low carbon cements are required. Nevertheless, also very important are the binder characteristics and how abundant the raw materials for the processes are. The authors [6] came to the conclusion that for all processes, except for CSA-clinker and BYF-clinker, a high abundance is assured. Since 1970, CSA cements have been largely used in China, with an estimated annual production of 2-3 Mt/a [7]. Calcium sulfoaluminate cements require both a higher Fe2O3 and a higher Al2O3 content in the raw meal, which could be partially satisfied by using bauxite residue.

In the Western World, CSA cements are manufactured for special applications by a number of cement producers, including Buzzi Unicem, Ciments Vicat and Holcim. Heidelberg Materials and Holcim developed belite-based CSA cements (BCSA) with the brandnames Ternocem and Aether. CSA cements are not classified as cements according to EN 197-1. Therefore, for an application in structural concrete these binders still need a technical approval in most cases. In China, belite-based low carbon clinker cements are also gaining importance [8]. In the last few years belite-rich Portland cement (RBPC) has been manufactured on an industrial scale. RBPC are classified as low heat Portland cements according to the standard GB200-2003. These cements are used as a type of low-energy, low-emission, high-performance cement with acceptable three- to seven-day early strength, 28-day strength equivalent to Portland cement and improved durability.

In autumn 2021, Schwenk Zement upgraded the installation of a pilot plant for the production of Celitement® (Figure 11) with a capacity of 1 t/d. The pilot plant is used for the process and product development, and provides material samples of different Celitement types for customer application tests [9]. The new cement binder is tested in various practical applications to provide a feedback for the market demand and the planned investment in an industrial plant. The first reference plant will have a capacity of about 50000 t/a. The installation has been scheduled for 2025. For 1 t of Celitement approximately 600 kg of high quality Ca(OH)2 and 400 kg of quartz sand are needed. The raw materials will be autoclaved in the same way as is known from the production of autoclaved aerated concrete (AAC). If pure raw materials low in Fe2O3 content are used, strictly white binder (L>90%) can be produced. However, after the tests are successful, the technology shall also be licenced to interested parties.

4 Production of calcined clay

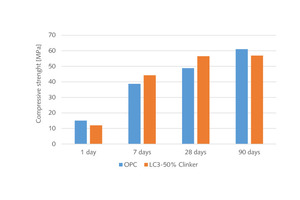

The calcination of clays for use in the cement and concrete industries has become a success story in recent years [10, 11]. An LC3 project that started in 2013 at the EPFL in Lausanne, Switzerland, shows that the synergetic reaction of calcined clay and limestone allows high levels of clinker substitution. LC3 is synonymous for limestone calcined clay cements. The LC3 family of cements allows 50% less clinker than OPC cement, 40% less CO2, similar strength development (Figure 12), better chloride resistance and resistance to alkali silica reaction. It has been shown that the main clay-size minerals such as kaolinite, illite, smectite, vermiculite and montmorillonite are available in all world regions. Clay can easily be activated, but the optimum activation temperature regime for each clay deposit has to be analysed. For the clay activation (calcination) either rotary kilns or flash calcination technologies can be used.

Flash calcining systems not only offer advantages in installation, operating and maintenance costs when compared to rotary kiln systems, but they additionally have a higher clay reactivity and therefore a larger degree of clinker substitution is achieved (35-40% for flash calcination and 20-25% for rotary kiln calcination). This trend can also be seen in the latest plant projects. New plants have become operational in the USA, Denmark, France, Colombia and Angola. Additional calcined clay plants will be installed in this and the next year in France, Portugal and Ghana. The projects show a trend to increasing plant capacities. While in former years most of the plant capacities have been below 0.1 Mt/a, plants of 0.4 Mt/a and even more are now being built. In India too, the first projects are now in the planning stage.

The pioneer companies in the last couple of years have been Argos in Colombia, Hoffmann Green Cement in France and Cimpor in Portugal. Cementos Argos invested 78 US$ million to build its first calcined clay unit at the Rio Claro plant (Figure 13) in Colombia. Construction started in March 2017 and the unit became operational in 2020, being at that time the largest such plant, with a capacity to produce 1500 t/h or 0.45 Mt/a of calcined clay. The raw clay is mined in the Altorrico mine, close to the Rio Claro plant. The average kaolinite content is 25-38%. Cementos Argos plans to produce 3.0 Mt/a of calcined clay by 2030. Future cement capacity additions will prioritize calcined clay projects. New projects in other geographies are on the horizon to open the company a path to their short, medium and long term goals.

Hofmann Green Cement is regarded as the pioneer in Europe for the design, production and distribution of low carbon cements with a carbon footprint as much as 6 times lower than traditional Portland cement. The company was founded in 2014 and opened a first production plant for low carbon cements in Bournezeau in Western France. At this site a second plant (Figure 14) with a capacity of 0.25 Mt/a has been commissioned. A third plant will be installed in 2024 in Dunkerque, France, to have a combined capacity of 0.5 Mt/a. Beside the H-EVA cement product, which is based on calcined clay and gypsum, Hoffmann Green produces 3 other patented low carbon cements. H-P2A is a geopolymer adhesive, which is based on a two component system containing activated clay and silicate. Anyhow, Hoffmann Green is licensing its technologies. In June 2023 it was announced that Hoffmann Green signed off an exclusive agreement with Shurfah Holding to build four Hoffmann units in Saudi Arabia.

Cimpor Global Holdings, which is part of the OYAK Group, installed its first calcined clay plant in Abidjan in Cote d’Ivoire. The plant has been operational since August 2020 and is known as the first greenfield integrated cement plant based on calcined clay (Figure 15). The capacity of the rotary kiln for calcined clay is 0.3 Mt/a and the cement production capacity of the plant is 2400 t/d. Cimpor ordered a second clay calcining plant for their location in Kribi in Cameroon.This plant will use the flash calcining technology. The capacity is 720 t/d of calcined clay and 2400 t/d of cement. Commissioning of the plant is scheduled for this year. In the last few years, Africa has become a hotspot for clay calcination. Another large plant will be installed in Ghana. This project is by CBI Ghana in Accra and involves installing the world’s largest gas suspension calcining system and 0.72 Mt/a calcined clay grinding capacity. Heidelberg Materials acquired a 50% stake in CBI to reduce the need for clinker imports into the region.

5 Outlook

New cements on the basis of a new clinker composition will have their market. To give an example: in China, about 2-3 Mt/a of CSA cements are produced every year. At the moment this corresponds to a market share of only about 0.1 to 0.15%. If the production of CSA cements continues at the same level, the market share could increase to 0.12 and 0.18% by 2030, because the Chinese cement production is expected to decrease. According to this, new cements will mostly only cover niche markets. But a huge impact can be expected from the production of calcined clays. This thermal activation could have very high market shares. It is too early to comment on whether a production level of 350 to 400 Mt/a will be possible by 2050, as projected by the IEA. There are some experts in the market who also see a potential in mechanical clay activation. OneStone Consulting plans to provide a multi-client report on the market for activated clays in autumn this year.