Latest trends in clay activation

Cementos Argos

Cementos Argos

HeidelbergCement

HeidelbergCement

OneStone Consulting

OneStone Consulting

![3 Global distribution of clay-size minerals [6]](/uploads/images/2021/w300_h200_x600_y831_Fig3_Mapping1L-1e99a414eff30b97.jpeg)

Enterprise Malet

Enterprise Malet

Cementos Argos

Cementos Argos

Hoffmann Green Cement

Hoffmann Green Cement

thyssenkrupp Cement Technologies

thyssenkrupp Cement Technologies

Aalborg Portland Holding

Aalborg Portland Holding

FLSmidth

FLSmidth

![10 Reactivity levels in clay calcination [7]](/uploads/images/2021/w300_h200_x550_y331_Fig10_Reactivity_NEU-da7b9f575e1d5414.jpeg)

Dynamis

Dynamis

thyssenkrupp Cement Technologies

thyssenkrupp Cement Technologies

thyssenkrupp Cement Technologies

thyssenkrupp Cement Technologies

thyssenkrupp Cement Technologies

thyssenkrupp Cement Technologies

![15 Projection of average global cement constituents [1]](/uploads/images/2021/w300_h200_x421_y297_Markets_Harder_Clay_Activation_Figure_15-c47649e376e7c68c.jpeg)

The cement industry is under pressure. The carbon footprint of the cement production has to be reduced significantly, the clinker ratio in cement has to be minimized but the availability of some of the mostly used supplementary cementitious materials (SCM) is already in a decline. Activated clays are a promising opportunity to close this gap because of their excellent pozzolanic properties and widespread availability. This article provides all important background information about clay activation, clay availability, market development and global projects, technical and economic aspects and how cement and concrete standardisation has to be adjusted.

1 Introduction

The cement industry has become one of the largest GHG polluters in the world [1]. Most of the 2.9 billion t CO2 emissions are generated in clinker manufacturing from the calcination/decarbonation of limestone (carbon carbonate), the key raw material. Today, in the cement production, these process emissions account for about 60% of total CO2 emissions, while still about 40% arise from the combustion of fuels required to generate the process heat (direct emissions) and from electricity generation for the grinding mills and other equipment (indirect emissions). Anyhow, the gross CO2 emissions per ton of cementitious material are in a decline, mostly due to alternative fuels and the substitution of clinker in cement. According to the Cement Sustainability Initiative (CSI) of the World Business Council for Sustainable Development (WBCSD) and the IEA (International Energy Agency) the gross CO2 emissions per ton cement have fallen from 752 kg/t in 1990 to about 653 kg/t in 2010 and 540 kg/t in 2018.

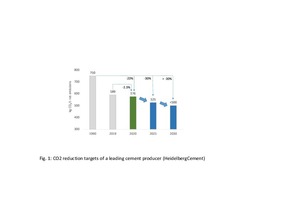

The CO2 emissions differ widely from region to region and cement producer to producer and depend very much on plant efficiencies, alternative fuel rates and clinker substitution rates. In recent years, the reduction of the carbon footprint has become a significant goal of the cement producers and the cement associations, respectively. Figure 1 shows for example the CO2 reduction targets of the HeidelbergCement Group, which is one of the leading cement producers. The net CO2 emissions were reduced from 750 kg CO2/t cementitious material by 23% to 576 kg/t in 2020. By 2030 it is intended to reduce the specific net CO2 emissions to below 500 kg CO2/t cementitious material. In 2020 HeidelbergCement achieved specific net CO2 emissions of about 155 kg CO2/m3 concrete. By 2050 a carbon neutrality for concrete is planned, which is in line with ambitions by Cembureau and the Global Cement and Concrete Association (GCCA) [2].

However, the future availability of clinker substitutes such as ground granulated blast furnace slag (GGBFS) from the iron & steel industry and fly ash from the power industry is uncertain [3]. Fly ash and GGBFS are also used directly in concrete to substitute cement. The European Ready Mixed Concrete Organization (ERMCO) provided figures for 2017 and 2018, which indicate that the average additions content in ready-mixed concrete (RMC) declined from 59.2 kg/m3 RMC to 55.8 kg/m3 RMC for the EU28 countries. Fly ash was the most widely used addition, followed by GGBFS, but in a few countries such as Austria and the Netherlands the supply was below the demand and fly ash had even to be substituted by GGBFS. Furthermore, statistics from the European Coal Combustion Products Association (ECOBA) show already a huge decline in the availability of fly ashes, due to the massive phasing-out of coal-fired power. By 2030, probably almost all of these plants will be closed in Europe.

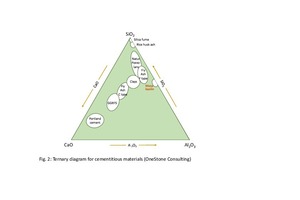

Accordingly, in Europe and elsewhere in the World, the cement and concrete industries have to look after other supplementary cementitious materials (SCM). Various natural and artificial SCMs which provide pozzolanic properties are used in different countries. These pozzolanic materials have variable siliceous or a combination of siliceous and aluminous contents (Figure 2). In a finely ground form and when moisturized these materials react with calcium hydroxide, to form compounds which have cementitious properties. Metakaolin is such a material. It can be produced when very pure clay minerals (kaolin) are heated in a certain temperature window between 600 and 900 °C to form an amorphous synthetic phase of the clay. If clay-like material is heated, we should call this “calcined” or activated clay. The activation of clays has been extensively researched in the last 10 to 15 years, which shows that up to 60% of cement could be replaced by such combined addition of activated clay and limestone with acceptable compressive strengths after 7 and 28 days [4, 5].

2 Clay minerals availability

Clay is one of the fundamental constituents of soils and accordingly it exists in the Earth’s crust and in sediments. The clay particles are formed through various geochemical and hydrothermal processes such as weathering and metamorphism. Typically, clay has spherical shapes with less than 2 m diameter. Clays are mixtures of different clay minerals such as kaolinite, illite, smectite, vermiculite and montmorillonite with other constituents and impurities such as quartz, feldspar, mica, iron oxide and other rock forming minerals. Figure 3 shows the global terrestrial distribution of the main clay-size minerals as a percent of the soil clay fraction (% clay). From the charts it becomes clear that the best topsoil and subsoil deposits exist for kaolinite and illite. However, the clay contents in these deposits is in best cases only between 30% and 60%. Higher quality clay deposits of more than 60% are used for the production of kaolin and performance minerals mainly in the ceramics and paper industries.

The annual availability of such secondary clay deposits for the production of activated clays is estimated by Scrivener and others [5] to be larger than the complete cement production. Activated clay is not only an environmentally-friendly clinker alternative, it can also save capital and operating costs and energy and can also bring benefits to the raw material supply in cement production. This is especially the case in those countries and regions where the reduction of CO2 emissions has a high priority and which have no or limited limestone deposits or where additives such as slag and fly ash are becoming increasingly scarce. Furthermore, with activated clay the cement production can be increased without increasing the clinker production. Activated clay can be used as a substitute for clinker in cement and also as a substitute for cement in concrete, due to its pozzolanic properties. A small disadvantage is that clay deposits vary largely from deposit to deposit so that in each case the clay mineral resources have to be analysed and tested before designing the plant and after the clay activation.

3 Market development and global projects

For several decades activated clays have been successfully used in the paper and board industries as a TiO2 extender. Such kind of structured clays are formed by heating relatively pure clay feed in rotary kilns at high temperature. The product which is highly reactive or which can have a high brightness is called Metakaolin. It is used in the paper, paint, ceramics, rubber and plastics industries. The product has prices that easily exceed 300 €/t and therefore finds only very limited applications as an additive in cement or high performance concrete. The global market for Kaolin and Metakaolin is about 42 million t per year (Mt/a) with China, the USA, Brazil, India and Germany with the highest production. Major producers include Imerys, BASF, Thiele Kaolin, Burgess Pigment Company, English Indian Clays Ltd (EICL), Poraver, Metacaulim do Brazil and several companies in China. One of the early activated clay system suppliers is the Australian FCT International with the first plant started in the 80th.

The first installation of a flash activated clay installation for the production of pozzolana for the cement industry was probably the 0.8 t/h pilot plant (Figure 4) in Toulouse, France in 1995. The plant was installed by Enterprise Malet, who also installed two other plants, a 10 t/h plant in Fumel, France and a similar plant in Surinam. Ash Grove Cement in the USA, which is now a subsidiary of the CRH Group, started to produce “calcined” clays in a rotary kiln around 1996 to provide a material that could reliably mitigate alkali-aggregate reactions. Ash Grove made this IP type Portland Pozzolan cement (according to the ASTM C150 Standard) from 3 different clay sources with brand name Duracem. Later fly ash was also mixed to the blend and the proportion of “calcined“ clay was reduced, to make the mix cheaper. Anyhow, Ash Grove Cement is still using “calcined” clays as an addition to cement or directly as an addition in concrete.

In 2001 Metacaulim do Brazil Indstria e Comércio Ltda was the first Brazilian company to produce and commercialize activated clay in industrial scale with 100000 t/a capacity plant. In the production, selected kaolinite clay is used and “calcined” at controlled temperatures. In partnership with the Laboratory of the Escola Politécnica of the University of São Paulo and the IPT-Institute for Technological Research of the State of São Paulo, Metacaulim provided several performance reports, which showed that the activated clays are in interesting option in the search of the improvement of the quality, the economy and the durability of Portland cement concrete. However, beside the concrete industry a significant quantity of the MetacaulimHP activated clay product is supplied to the refractories and ceramics industries, metallurgy of iron and steel, chemical and other industries.

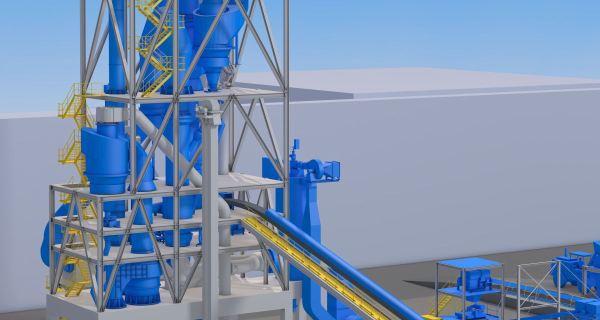

Since 2009 Cimento Planalto (CIPLAN) is operating a rotary kiln for the production of activated clays in their Sobradinho cement plant in the vicinity of Brasilia, Brazil. The clay activation plant has a capacity of 600 t/d and uses a rotary kiln with 3 m diameter and 52 m length. Supplier is Dynamis from São Paulo. In 2018 Dynamis recieved a 2nd order for a new pozzolan production line from Cementos Argos in Colombia at their Rio Claro site. The plant (Figure 5) has a capacity of 450000 t/a (1500 t/d clay activation), started operation in April 2019 and comprises the Dynamis D-Pozzolan “calcined” clay technology with flash dryer and rotary kiln. The “Green” cement from Argos reduces up to 38% of CO2 emissions when compared to OPC. CIPLAN has been acquired by the Vicat Group in January 2019. In 2019 Vicat also launched the plan for the partial replacement of clinker in several countries by thermally-activated clays and limestone filler. A first project is the ARGILOR project at the Xeuilley site in France.

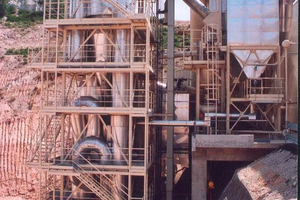

In November 2016 Argentina’s Cementos Avellanda (CASA), which is part of the Votorantim Cementos Group awarded China’s TCDRI (Sinoma Group) with cement plant modification contract to produce “calcined” clays at the Olavarria site. One of the two kilns of the site needed to be modified as well as cement mill #8, where the pozzolana is added as an additive. CASA is a pioneer in the Argentine cement industry in supplying such type of cement. In Europe, Hoffmann Green Cement Technologies (HGCT) is probably the first company to start commercial production of activated clay for the construction industry. Since November 2018 HGCT operates a 50000 t/a pilot plant in Bournezeau, Vendée/France. This plant produces a green cement, reducing CO2 emissions to 200-250 kg/t, according to the company. Now, HGCT is in the construction process of a second plant (Figure 6) at its site in Bournezeau with 250000 t/a capacity to be commissioned in 2022. By 2025 another line is planned to have a total capacity of 550000 t/a.

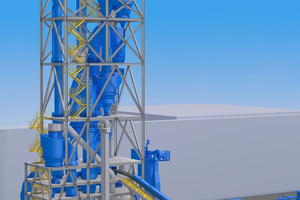

Cimpor Global Holdings (CGH), which is part of the Turkish Oyak Group has installed in Abidjan, Ivory Coast, the first Greenfield “calcined” clay integrated cement plant. The plant has a capacity of up to 300000 t/a of calcined clay and 2400 t/d cement grinding and was commissioned by the Portuguese supplier IPIAC-Nery in August 2020. The main machinery comprises a rotary dryer, rotary kiln and cooler. In the meanwhile, the original design of the clay calcination line has been replaced and revamped due to inefficiencies and deficiencies. CGH ordered from thyssenkrupp Industrial Solutions a 2nd clay activation plant. The new plant will have a capacity of 720 t/d calcined clay and 2400 t/d “Green” cement and will be installed near the Cameroon Sea Port of Kribi. This time a flash clay activation technology (Figure 7) will be used. When completed in spring 2022, the plant is expected to save 120000 t/a of CO2 emissions compared to a standard OPC cement.

In June 2021 FLSmidth received an order by Vicat to supply a clay activation line for their Xeuilley integrated cement plant in France. The order is for flash technology with a minimum of 400 t/d activated clay with environmental control and alternative fuel firing system. The new production line has a design capacity of 525 t/d activated clay and is scheduled to be commissioned in 2023 and will probably be the 2nd full-scale clay activation plant in Europe. Another plant is planned by Cementir Holding. The Cementir Group is in a transition to “Green” cement. In January 2021 their new low-carbon cement, named Futurecem, was launched. It is assumed that the 1st industry-scale clay calcination plant of Cementir will be installed at Aalborg Portland Holding (Figure 8) in Denmark. Over the last few years several tests with calcined clay from a pilot plant of FLSmidth showed that Futurecem concrete works well with fly ash and that higher CO2 savings higher can be achieved than with fly ash alone.

4 Important technical and economic aspects

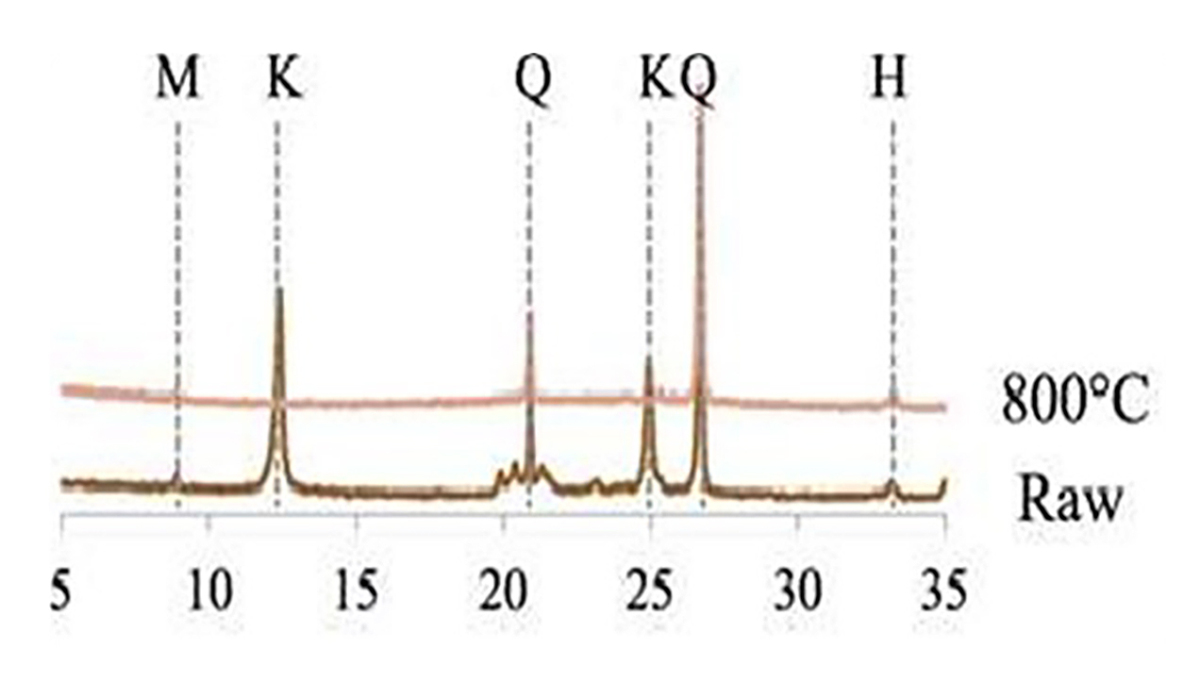

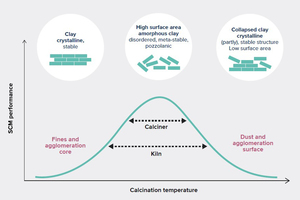

Clay is easy to activate but the optimum activation temperature regime for each clay deposit has to be analysed. Applying a conventional rotary kiln for clay activation, might lead to a less reactive activated clay compared to a flash “calciner”, impacting the final substitution rate of activated clay in the cement negatively. Reason for that is the flame physics in conventional rotary kilns, which is leading to a wide temperature distribution. In combination with a relatively long retention time in the rotary kiln, the clay is partially heated upon the optimum activation temperature leading to partial recrystallization effects and a loss of activity. Figure 10 shows the different reactivity levels for clay calcination using a flash “calciner” and rotary kiln (soak technology), by analysing the reacted calcium hydroxide (CH) [7]. About 80% of the CH reacted after flash activation, while only 40 – 60% reacted after rotary kiln activation. At higher activation temperatures this effect is becoming worse

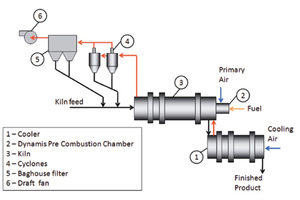

Up to now, the most widely used clay and kaolin calcining technology is based on rotary kilns. Figure 11 shows an advanced system as it is designed by Dynamis. The system is capable of drying, activating and cooling the material. The clay raw material with moistures of more than 20% is directly fed into the kiln, where the material is dried, heated and activated with temperatures up to 900 °C. The kiln is equipped with specially designed lifters to improve the heat and mass exchange in the kiln. Clay cooling is in a separate rotary cooler which also heats the combustion air. A rotary cooler is used instead of a grate cooler, due to the relatively low outlet temperatures of 120 °C. The advantage of a rotary kiln calcination is that existing kilns can be retrofitted, low material preparation is necessary and that a broad range of conventional and alternative fuels can be used, included petcoke. However, the sensitivity on the process control is relatively low and a separate material preparation step might be needed in order to achieve acceptable colour control results.

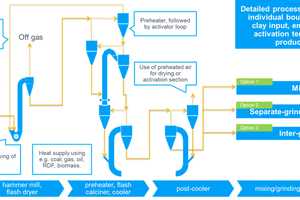

Figure 12 shows a standard flash activation process flowsheet as it was developed by thyssenkrupp Cement Technologies. The activation system comprises a 2-stage clay preheater, followed by an activator loop and cooling system. The actual plant design depends on the individual boundaries of the plant. Influencing parameters are e.g. the raw material quality (moisture; minerals to be activated, impurities, etc), local emission limits, fuels (conventional/alternative fuels) and the optimum activation temperature to achieve the best reactivity of the activated clay for highest clinker substitution rates. To find the optimum design, LAB tests serve as a starting point for customer projects. Additionally, raw clay can be activated in different flash activation facilities (up to 500 kg/h) to prove the operation with the intended clay source as well as its colour and product quality.

The activated clay can either be mixed directly with cement or concrete or has to be ground separately or by intergrinding with other constituents. The process allows the use and full activation of mixed-clay raw materials and the use of a large number of conventional and alternative fuels including biomass with the target to lower the operational costs and CO2 emissions. For the production of high quality activated clays raw material clay purities of 40% are sufficient. For lower quality active clays even lower clay purities can be used. A too high clay purity could have a negative effect, because of difficulties in the product handling. Due to the precise temperature steering, short process retention times and a heat recuperation from the cooler to the drying or to the activation section, highly reactive clay and lowest fuel consumption rates can be achieved. The colour of the clay can be adjusted individually by applying different technologies.

The pozzolanic activity mainly depends on the amount of amorphous silica and alumina in the composition of the pozzolanic material. Nevertheless, it is also influenced by the specific surface area and particle size distribution beside other parameters. Up to now X-ray fluorescence (XRF) and X-ray diffraction (XRD) are the main automated test methods that give an initial idea about materials as potential pozzolans by the determination of silica and aluminium oxide in composition (by XRF) and by the determination of the amorphous phase (by XRD). Now with the polabCal solution from thyssenkrupp Industrial Solutions, there is a direct instrumental solution (Figure 13) for the product reactivity measurement in clay calcination. Thyssenkrupp Industrial Solutions and Calmetrix have partnered to develop polabCal, the first automated calorimeter for laboratory automation in the cement industry [8]. The system provides rapid, accurate and numeric information on cement, clinker and calcined clay reactivity, so that data can be fed back to the production process for optimization. Any changes in the calorimetry curve can be attributed to a change in reactivity.

A number of concept studies have been made by suppliers to compare the two different clay calcining systems (Table 1). Flash calcining systems not only offer advantages in installation, operating and maintenance costs when compared to rotary kiln systems, additionally also a higher clay reactivity and therefore a larger degree of clinker substitution is achieved (35-40% for flash calcination and 20-25% for rotary kiln calcination) [7]. For investors the shorter pay-back period of about 3-3.5 years for flash clay calcination systems is another strong point. Investment costs for new flash calcination lines including the grinding system have been in the range of 60-70 €m/1000 t/d. The economy of scale for such flash calcination plants with standard sizes in a range of 500 to 1000 t/d (200000 – 350000 t/a) is comparable to cement plants of the same size, but still low when compared to conventional clinker production lines of 10000 t/d (3.5 million t/a) and above.

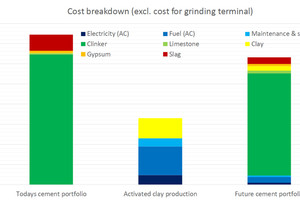

According to a study in 2007 by the European Cement Research Academy (ECRA) the unit investment costs for new integrated cement plants with capacities of 2.0, 1.0 and 0.5 million t/a, using state-of-the-art technology (conventional dry process with 5-stage preheater and calciner) are about €130/t, €170/t and €250/t, respectively. The International Energy Agency (IEA) analysed in 2010 that the investment cost for a 1.0 million t/a integrated cement plant will increase to some €560/t if post-combustion technologies are used and the CO2 emissions produced in the process are captured (and stored) or the costs will increase to some €325/t if oxy-combustion technologies are used. Therefore, the clay calcination has tremendous advantages in the capital costs, but operating costs can also be reduced. Figure 14 illustrates possible cost savings in cement production for the region of West-Africa. Basis for this scenario is an upgrade of an existing grinding terminal (1.2 million t/a) by an activated clay line. The target is to optimize the cement production costs at the same cement output and comparable cement quality. Since the output capacity will remain the same, specific grinding costs are in the same order of magnitude for both scenarios and will therefore not be considered in the cost breakdown.

The average production costs before optimization are at 37.2 €/t of cement. The production costs for activated clay are calculated to 16.5 €/t of activated clay. After adapting the cement portfolio, the average production costs are at 31.5 €/t. This results in savings per year of around 7 million € at constant cement production. A significant cost driver in this scenario are the clinker costs. In the case, that the clinker costs are higher as the assumed 40 €/t DAP, the business case will be even more attractive. A clinker price of e.g. 50/60 €/t DAP will lead to savings of around 9 to 11 million € per year if all other boundaries are constant. Another business case lever would be an increase of the cement output. In case of a bottleneck of the existing grinding terminal, the capacity has to be boosted efficiently (low CAPEX) or new capacity has to be built (higher CAPEX). The boundaries for the calculated business case are illustrated in Table 2 and have to be adapted to the individual case.

5 Cement & concrete standardisation

Standardisation is some kind of a barrier to the introduction of LC3 cements. The majority of the Standards used in the world regions are prescriptive, this means they dictate the composition that can be used.The most widely used norms for cement are the American ASTM- C1157 Standard for Hydraulic Cements and C 595 for Blended Cements, originally approved in 1992, and the European EN 197-1 Standard, which is from the year 2011. It is state-of-the-art, that highest clinker substitution rates in cement can be achieved, when activated clay is mixed with limestone and clinker. Such limestone, calcined clay cements – or LC3 – can vary in the composition with up to 50% clinker, 30% activated clay, 15% limestone and 5% minor additional constituents including gypsum. Such LC3-50 (50% clinker) cements still have a similar or even better 7-day and 28-day strength than conventional Portland cement and better chloride resistance and alkali-silica (ASR) resistance.

In the ASTM Standards ternary blends of calcined clay (natural pozzolans) and limestone are allowed. These pozzolans can either be interground with Portland cement clinker and gypsum to produce a Type IP blended cement or they can be ground separately as mineral admixtures for concrete. The products are produced under the specification requirements of ASTM C 1157 and ASTM C 595 for hydraulic and blended cements or ASTM C 618 for mineral admixtures, respectively. In ASTM C 618 (mineral additives in concrete), the classification for raw or calcined natural pozzolans is Class N. In the ASTM Standards, calcined clay can be added according to the pozzolan reactivity. However, the existing DIN EN 197-1 Cement Standard, does not allow such high ternary blends with clay and limestone. While CEM II Portland-composite cement (CEM II/C-M) only allows up to 20% limestone and zero% natural calcined clays, CEM IV Pozzolan Cement (CEM IV/B) allows up to 55% natural calcined clay, but zero% limestone.

CEM VI Composite cements allow up to 20% limestone but don’t allow any natural calcined constituents. At the moment limestone-calcined clay cement is only allowed in the European cement standard CEM II/A-M and CEM II/B-M with minimum clinker content of 65-80% and limestone and calcined clay at a maximum rate of 12-35%. Accordingly, still today the potential CO2 reduction is limited by the minimum clinker content in Portland-composite cements. After introducing the EN 197-1 as harmonized standard, the European Committee for Standardisation (CEN/TC 51) decided to amend the standard to include new cements. For that purpose, an amendment of the mandate was necessary. This process started already in August 2015, and in 2018 a proposal of revised Mandate M 114 (for cements) was sent to CEN by the Commission [9]. However, beside the initiation of the revision up to now no revision of the existent Cement Standard was made and no new standard was released.

With the introduction of Phase 4 of the EU Emissions Trading Scheme in January 2021 it is required by the cement producers that the EU should work with standardisation bodies to ensure the timely adoption of product standards to allow low-carbon cement and concrete to be put on the market. The European Standardization Committee is still working on widening the range of common cements within the scope of EN 197-1 and allow CEM II/C Portland Composite cements including ternary cements with activated clay and limestone. If this procedure will not be successful the alternative is the leave the EN 197-1 (2011) as it is currently, and to draft new non-harmonised nationwide Standard that covers ternary cements to be included in a new EN 197-5 Cement Norm. Furthermore, the use of calcined clays as a concrete additive requires a national building authority approval either through proof of performance via the equivalent w/c value or a binding agent approval according to the “performance concept” such as outlined by the German Institute for Structural Engineering.

6 Market outlook

Clay calcination can become a success story in the cement industry to reduce the carbon footprint. To understand the market potential, projections by the IEA Technology Roadmap on the Low-Carbon Transition in the Cement Industry can be used. Figure 15 shows the estimates of the global average cement composition in the year 2014 and the projections for the year 2050 under the 2°C climate scenario [1]. In the projection it is estimated that in 2050 about 8% of the global average cement constituents will be calcined clay and that the global cement production is 4680 million t/a, which results in a production of 375 million t/a calcined clay. This will require an installation base of almost 470 million t/a, if the capacity will be utilised by 80%. Until 2021 only 5 million t/a is the cumulated installation capacity from the identified projects. So by 2050 another 465 million t/a of calcined clay capacity or almost 70 new lines per year (each with 1000 t/d) have to be installed.

Not necessarily, all the new capacity needs to be completely new installed. There is definitely a room for the modification of existing cement plants with preheaters and rotary kilns, which can be used for the production of calcined clays. Anyhow, such conversions will also require capital investment for the adaption of alternative fuels and the colour adjustment of the finished product from reddish to grey. At the end maybe 50-70% of the investment costs for the plant can be saved, but the operating costs of the plant can be 20-30% higher than a new-build flash calcining plant. Furthermore, it has to be considered that the reactivity of the activated clay from rotary kiln plants is significantly lower than that from a flash calcination and accordingly the product quality will be lower, which will also reduce the clinker substitution in the cement and the possible CO2 savings.