Next-generation carbon capture technologies for cement industries

tkIS

tkIS

OneStone Consulting

OneStone Consulting

Calix Limited

Calix Limited

OneStone Consulting

OneStone Consulting

Svante Inc.

Svante Inc.

Chart Industries

Chart Industries

![6 Calcium looping (CaL) carbon capture [8]](/uploads/images/2022/w300_h200_x600_y371_Fig6L_CaL-9b173befdf8063c9.jpeg)

tkIS

tkIS

OneStone Consulting

OneStone Consulting

![9 Oil and gas underground reservoirs [11]](/uploads/images/2022/w300_h200_x600_y269_Fig9L_Reservoirs-3dadd03f23202450.jpeg)

HeidelbergCement

HeidelbergCement

Aker Carbon Capture

Aker Carbon Capture

Holcim Deutschland

Holcim Deutschland

Raffinerie Heide

Raffinerie Heide

Holcim Group

Holcim Group

OMV Group

OMV Group

Cemex

Cemex

Worldbank

Worldbank

Carbon capture, utilisation and storage (CCUS) technologies are important as well as necessary in meeting the net zero CO2 targets of the cement industry by 2050. Accordingly, projects on carbon capture from the exhaust gases of cement kilns have accelerated in the last few years. This market review gives an overview of the most promising next-generation carbon capture technologies for the cement industry with examples on advanced projects including the utilisation and storage of CO2.

1 Introduction

According to the International Energy Agency (IEA), we are approaching a decisive moment for international efforts to tackle the climate crisis. In its ‘Net Zero by 2050 Scenario’ [1], the IEA sees the need for globally 1700 million t per year (Mt/a) CO2 capture by 2030 and about 7000-8000 Mt/a of CO2 by 2050. The current market size of carbon capture projects is just around 40 Mt/a (of which more than 70% is from natural gas processing, 17% from synfuels and hydrogen processing and 6% from power generation). Accordingly, a substantial increase of carbon capture projects is required. The cement industry, which is one of the largest global CO2 emitters accounting for about 6-7%, is one of the major targets. With each t of clinker manufactured from the limestone raw material (CaCO3), the default value of 0.525 t of CO2 is unavoidable and is released from the calcination process [2].

With a global cement production of about 4.31 billion t in 2021 and an average global clinker factor of 0.72 (increased from 0.70 in 2019), about 1629 million t per year (Mt/a) of CO2 were generated in clinker manufacturing just from the decomposition of the raw material. In cement plants about 60% of the emitted CO2 is process CO2 [3], the remaining portion originating from burning fossil fuels. While the CO2 from fossil fuels can be reduced by burning carbon-neutral biofuels, only a small amount of the process CO2 can be saved if the amount of CaO in the clinker is further reduced, e.g. by using alternative decarbonated raw materials or by using new types of cement clinker such as sulpho-aluminate clinker (SAC), ferro-aluminate clinker (FAC) or other materials [2]. Accordingly, carbon capture, utilisation and storage technologies are required to achieve the carbon neutrality targets of the cement industry.

2 Carbon capture technologies

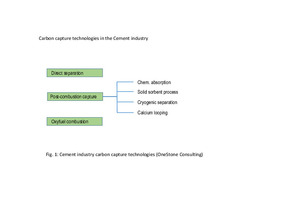

It has to be noted that due to the relatively high CO2 concentration of the cement kiln off-gas the conditions for carbon capture in the cement industry are more favourable than in most other industrial applications. However, due to the higher “pollution” of the cement kiln exhaust gas, some of the prospective carbon capture measures introduced in other industries have a limited practicability. In principle, three basic carbon capture technologies can be used by the cement industry (Figure 1): Direct separation, post-combustion capture and oxyfuel combustion, which have all achieved next-generation status in the cement industry. The post-combustion technologies, which are also called “end-of-pipe” technologies, can be further differentiated. In the cement industry four technologies will find their application: chemical absorption processes, solid sorbent processes, cryogenic separation and calcium looping. The latter can be regarded as a specific solid sorbent application.

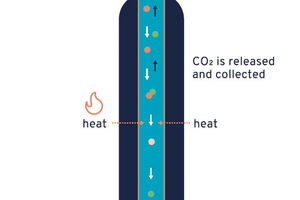

In the direct separation process, a special reactor replaces the conventional calciner to separate the process CO2 from the limestone calcination. The technology is based on an indirect heating of the cement raw material via a special steel tube within the calciner (Figure 2). The advantage is that the pure process CO2 can be captured as it is decomposed from the CaCO3, while the furnace exhaust gases are kept separate. The system can be applied to existing and new kilns and the carbon capture requires no additional use of heat or any other commodities. In 2015, the technology was introduced to the cement and lime industry by the Australian Calix Limited under the project name LEILAC (Low Emission Intensity Lime and Cement project) as a cost-effective technology for carbon neutral industrial production [4].

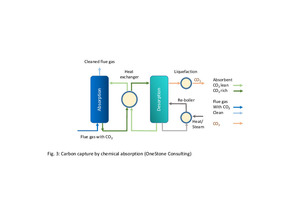

Post-combustion carbon capture can principally be adapted to any combustion or CO2 producing process. Several different technologies have a large potential in the cement industry [5]. One of the most promising processes is chemical absorption. Gas separation by absorption is based on the principle that the CO2 in the flue gas can be absorbed in a liquid solvent (absorbent), while the other gas particles are released with the clean flue gas (Figure 3). After separation, the CO2 is liquefied and stored and the solvent is recovered in a subsequent stripping or desorption unit. There are several system suppliers for the cement industry, including Norway-based Aker Carbon Capture and UK-based Carbon Clean, which either use high-performance proprietary solvents or modularized special reactors, or a combination of both.

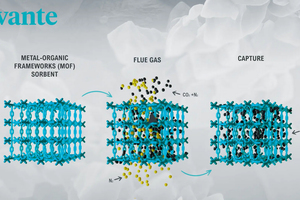

Adsorption-based post-combustion carbon capture is a promising technology for capturing CO2 emissions from cement kilns, due to the ease of adsorbent regeneration in comparison with solvent-based technologies. One of the most promising technologies uses solid adsorbents with an extremely high CO2 storage capacity. These are tailor-made nano-materials and structured in metal organic frameworks (MOF) (Figure 4). A sugar-cube sized quantity of these nano-materials has about the surface area of a football field. The MOF technology that has been introduced to the market by Canadian-based Svante Inc. (formerly Inventys) allows rapid desorption cycles and is robust with regards to steam, O2 and acidic gases such a NOX/SOX, which make it ideal for the cement CO2 capture application [6]. Another technology provider is MOF Technologies.

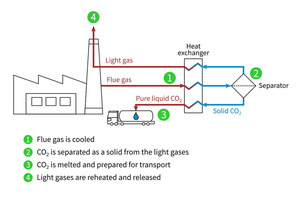

Cryogenic carbon capture (CCC) is an easy to retrofit post-combustion technology that utilises cryogenic conditions to separate CO2 from the other off-gases in the cement plant. In the CCC concept of SES (Sustainable Energy Solutions by Chart Industries) the CO2 is frozen out from the kiln exhaust gases and the solids are separated from the gases prior to being vented to atmosphere (Figure 5). The CCC technology is able to remove >98% of the CO2 as well as NOx, SOx and other pollutants [7] and is therefore a suitable method to simplify the cement exhaust gas cleaning.

Another method for carbon capture is calcium-looping (CaL), which comprises a carbonator and calciner (Figure 6) and is based on the reversible reaction between CaO and CO2 at high temperatures. CO2-rich gases from the preheater are fed into a carbonator, where they come into contact with CaO-rich solids. The solids formed by the carbonation reaction with CaCO3 are sent to the calciner for regeneration at temperatures above 900 °C [8]. One technology provider is the Italian Laboratorio Energia Ambiente Piacenca.

In the oxyfuel method, pure oxygen replaces ambient air in the clinker production process. As the nitrogen content of the air is no longer present, the CO2 concentration in the kiln exhaust gas can be increased to up to 100%. Accordingly, an efficient CO2 separation can be used for the downstream utilisation or storage of carbon dioxide. ThyssenKrupp developed the 2nd oxyfuel generation, where complex exhaust gas recirculation, as envisaged in the first-generation oxyfuel process, is completely eliminated (Figure 7) [9]. The gas volume in the clinker burning process is considerably reduced. For cement producers, the 2nd generation will allow reduced investment and operating costs. However, an air separation unit (ASU) has to be added to the process to provide the pure oxygen and ambient air has to be provided for cooling the clinker.

3 CO2 utilisation and storage

Technologies for the use of CO2 in the production of fuels, chemicals and building materials are generating global interest to support investment in CO2 capture technologies. However, according to the IEA only about 250 Mt/a CO2 are used by different industries up to now [10]. 57% goes into the production of fertilizer (urea), 31% is for enhanced oil recovery (EOR), 6% for food and beverage and only 6% for all other industries, incl. chemical and metal industries. Figure 8 gives an overview of the most prospective CO2 utilisation and storage pathways for the cement industry. Because most of the CO2 conversion technologies are highly energy extensive and very costly and direct use is limited, the future scale of CO2 use is highly uncertain. Accordingly, CO2 storage has been highlighted by the IEA as a critical part of the portfolio of technologies needed to achieve climate goals.

CO2 can be used to produce some of the fuels/chemicals available on the market today, such as methane, methanol and similar products. With hydrogenation, CO2 can be directly converted to methanol (CH3OH). The price and availability of hydrogen is of major importance. E-methanol or renewable methanol is produced by hydrogen from water electrolysis using electricity from renewable sources, combined with CO2. Low-carbon methanol (recycled carbon methanol) can be produced by hydrogen from by-product or waste gas, processed and combined with CO2. In indirect conversion processes CO2 is first converted into CO and then followed either by a Fisher-Tropsch (FT) process or methanol synthesis process. However, while the latter processes are very energy intensive, processes on the basis of e-methanol and recycled carbon methanol have already proven to be efficient. One leading technology provider is the Iceland-based Carbon Recycling International with a 110000 t/a methanol project in the steel industry in China.

Sequestration of CO2 by mineral carbonation offers a promising potential. The method is also referred to direct CO2 use. CO2-cured concrete is one of the most mature applications of CO2 use. CO2 can also be used in the production of building materials e.g. to replace water in concrete or as a raw material in its constituents (cement and construction aggregates). Taiheiyo is one of the companies that has made several successful tests with CO2 sequestration in demolished concrete, concrete sludge, precast concrete products and ready-mixed concrete. For the CO2 mineralization a specially designed carbonation reactor has been used. CO2-cured concrete can have a superior performance, lower manufacturing costs and lower CO2 footprint than conventional concrete. However, qualifying the market potential is difficult.

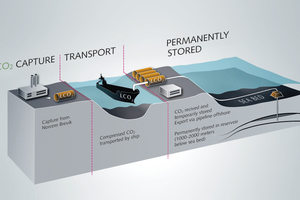

While today the use of captured CO2 is prioritized, excess quantities can be safely stored in suitable underground geological formations, either on-shore or off-shore and mostly in depleted oil and gas reservoirs or saline aquifers (Figure 9). A report by the Intergovernmental Panel on Climate Change (IPCC) concluded in 2005 that carefully selected and managed geological reservoirs are ‘very likely’ to store over 99% of the sequestered CO2 for longer than 100 years and ‘likely’ to retain 99% of it for longer than 1000 years. By 2019, only 19 such large-scale reservoirs have been operated globally with CO2 injection, of which four are in saline formations (Sleipner, Snovit, Quest and IBDP). A recent analysis indicates that 10 to 14 thousand CO2 injection wells will be needed globally to achieve the 2DS goal by 2050 [11]. Because most of these wells are not close to the cement plants, CO2 has to be liquefied and frequently transported over long distances.

4 Advanced projects in the cement industry

There are already a large number of carbon capture projects in the global cement industry. While most of the projects are in a testing or pilot state, a few are industrial scale demonstration plants. Up to now, the majority of the projects are in Europe, however there is almost at least one project in the major cement producing countries around the world. Here, the major advanced projects are highlighted.

4.1 LEILAC project

There are two pilot cement plant projects which aim to apply and demonstrate the DSR (Direct Separation Reactor) breakthrough technology that will enable Europe’s cement and lime industries to reduce their carbon footprint significantly. The LEILAC1 project, a CO2 capture pilot installation with a capture capacity of 25000 t of CO2 per year has been developed at HeidelbergCement’s Lixhe plant in Belgium (Figure 10). The LEILAC2 installation at HeidelbergCement’s Hanover plant will be capable of capturing 20% of the cement plant’s CO2 emissions, corresponding to around 100000 t of CO2 per year. The project will pass the detailed design phase in 2022, which will be followed by procurement and plant construction in 2023. Extensive tests shall be finalized in March 2025. The LEILAC consortium is led by the LEILAC Group (technology provider Calix), and comprises HeidelbergCement, CEMEX, Cimpor, IKN, Lhoist, and others. CO2 capture costs are expected to be 46 to 62.5 €/t CO2 [12].

4.2 Norcem’s Brevik CCS project

With 400000 t of CO2 to be captured per year and transported for permanent storage, HeidelbergCement will install the cement industry’s first industrial-scale carbon capture and storage (CCS) project at Norcem’s Brevik plant. A feasibility study for the project already started in 2016. An investment decision by the Norwegian Parliament was made in December 2020. The total costs (investment and operating costs) for five years are estimated at NOK 11.2 billion (€ 1.1 billion). The carbon capture facility will use advanced chemical absorption technology supplied by Aker Carbon Capture and is scheduled to be fully operational in 2024. Figure 11 shows an illustration of the planned CCS-project. CO2 will be transported by ship from the Brevik plant to an onshore facility on the Norwegian west coast for intermediate storage. Then it will be transported via a pipeline to a subsea storage formation in the North Sea (Atlantic).

4.3 Second generation Oxyfuel projects

The first two demonstration projects of the European cement industry were released in Jan. 2018 at Lafarge’s Retznei cement plant in Austria and the Collefero plant of Italcementi in Italy. With its latest CI4C (Cement Innovations for Climate) project in Mergelstetten, Germany, HeidelbergCement is investing in a pre-industrial large-scale oxyfuel project (Figure 12), which will enable the later use of CO2 as a raw material for so-called reFuels. The project partners HeidelbergCement, Buzzi Unicem - Dyckerhoff, Schwenk Zement and Vicat have commissioned TKIS to build a polysius® pure oxyfuel kiln system at the cement plant in Southern Germany. With the 2nd generation of these plants, recirculation of exhaust gas can be eliminated.

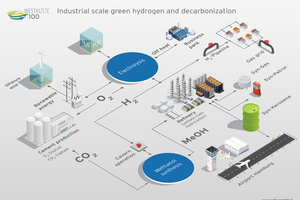

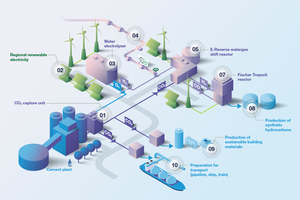

At its Lägerdorf cement plant in Northern Germany, Holcim Deutschland will install another 2nd generation oxyfuel kiln from thyssenkrupp, which uses an air separation unit to supply oxygen directly. The new CCU system will provide captured CO2 to a hydrocarbons plant, which will produce methanol for other industrial applications. The plant will have a capacity of 1.2 Mt/a CO2 and will make Lägerdorf one of the world’s first carbon neutral cement plants. The project is integrated in “Westküste 100” (Figure 13), which is a complete coupling of cement, energy and chemical sectors that beside the CCU plant will provide green hydrogen from renewable energies for methanol production and the H2 gas grid.

4.4 Holcim’s other CCU projects

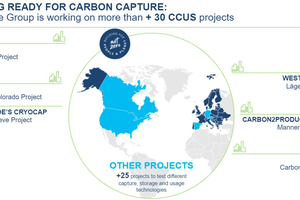

Today the Holcim group is working on more than 30 CCU/CCUS projects (Figure 14). A CCU demonstration project is now in its second phase at Lafarge’s Richmond cement plant in British Columbia/Canada. Exhaust gas from the cement kiln is captured via Svante’s solid absorbent technology. The CO2 will be used for low-carbon fuels and CO2 concrete. In October 2021 Lafarge and Svante achieved a 1000h milestone with a CO2 recovery of 85% and a CO2 purity of 95%. The project was initially installed by LafargeHolcim in partnership with Total and Inventys and was fully operational by the end of 2020. Now, a second CO2MENT project is being installed in Holcim’s Portland cement plant in Florence, Colorado/USA.

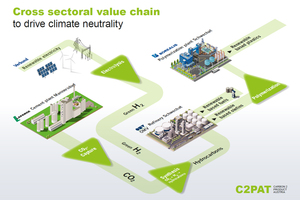

In June 2020, Lafarge Zementwerke, a member of the Holcim Group, OMV Group, Verbund and Boreal co-signed a Memorandum of Understanding (MOU) for the joint planning and construction of a full-scale CCU plant by 2030 to capture CO2 and convert it into products (Figure 15). The project shall be completed in three phases. Eventually, almost 100% of the 700000 t/a of CO2 emitted from LafargeHolcim’s cement plant in Mannersdorf will be captured. Green hydrogen (from renewable energies) will be produced by Verbund, the captured CO2 will be transformed by OMV to renewable-based hydrocarbons, which, in turn can be used to produce renewable-based fuels or be utilised by Borealis as a feedstock to manufacture value-add plastics.

4.5 Carbon Clean chemical absorption projects

For its Carboneras cement plant in Spain, Holcim will use the Carbon Clean chemical absorption process. The installation will initially capture 10% of the 700000 t/a of CO2 emissions from the plant. In 2020, Cemex Ventures entered into a collaboration agreement with Carbon Clean to jointly develop and implement carbon capture technologies across Cemex’s cement operations, starting with a carbon capture project at the Victorville cement plant in the USA. In Germany, they are working on a carbon capture project at the Rüderdorf cement plant. The initial stage of this project aims to capture 100 t/d of CO2 at the plant and combine it with hydrogen from renewable resources to produce green synthetic hydrocarbons (Figure 16). The major project partners beside Cemex and Carbon Clean are Enertrag as renewable energy provider and Sasol ecoFT as the producer of e-kerosene. Dalmia Bharat is developing another carbon capture project with Carbon Clean at their Tamil Nadu cement plant in India.

4.6 Cryogenic Carbon Capture

FLSmidth has signed an agreement with Chart Industries to implement advanced carbon capture technology to significantly reduce CO2 emissions from cement production. Chart is a provider of Cryogenic Carbon Capture® (CCC) technology. In October 2021, the U.S. Department of Energy (DOE) awarded US$ 5 million in funding to design, build, commission and operate an engineering-scale CCC process at Central Plains Cement Co.’s cement plant in Sugar Creek, Mo., which is a wholly-owned subsidiary of Eagle Materials. The project will scale the CCC system to a capacity of nominally 30 t/d of CO2 with the intention of demonstrating that it captures more than 95% of the almost pure CO2 from the kiln exhaust gas stream.

5 Outlook

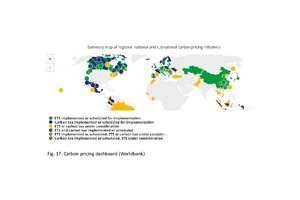

Carbon pricing initiatives are increasing around the world (Figure 17). At the moment prices are highest at the European Carbon Credit Market with around 85 €/t CO2, followed by New Zealand with around 75 $/t CO2. However, there are other markets where the prices are much lower, such as those in South Korea or China, or countries where the carbon markets have only been partly developed. For a fair competition is important that the carbon markets will be globally aligned. In Europe the increasing carbon prices mean that some of the carbon capture technologies are already becoming competitive.

Detailed technological-economic studies between costs per t CO2 captured and costs avoided have been made for some of the next-generation technologies [12]. The cost comparisons depend to a large extent on energy penalties, which take into account the higher fuel consumption of carbon capture technologies and corresponding higher CO2 emissions. Last but not least, due to the fact that CO2 transport and storage technologies cost the same or even more than carbon capture technologies utilisation technologies are in the focus.