European construction equipment industry staged a grand comeback in 2021

The CECE Annual Economic Report shows that the demand for construction equipment in Europe stayed on a growth path in 2021, after the industry had already seen a return to growth in the second half of 2020 when the impact of the pandemic was receding. Demand benefitted from a combination of stable performances by different end-user segments and pandemic stimulus measures, whose potential fully unfolded in 2021. On the other hand, the construction equipment industry also experienced the most severe supply-chain disruptions in recent history, in particular shortages of raw materials and components, as well as scarce and expensive freight transport.

“Against this backdrop, the 24% increase in sales in 2021 on the European market is a remarkable outcome. The European construction equipment industry is indeed resilient as shown over the last two years. The continued increase in demand in our largest markets, the European recovery programme and the global construction boom are boosting our business”, said Alexandre Marchetta, CECE President, opening the CECE Press Conference on March 3rd 2022.

The figures surely include a statistical “base effect” of yearly comparison, with the enormous drop of the first pandemic lockdown in 2020. However, after weathering the Covid crisis, underlying demand within the industry has remained strong and is on track to close the gap with record sales levels of 2007.

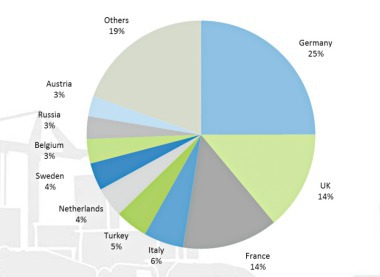

2021 saw consistent trends across the equipment sub-sectors with all product segments recording growth in sales of between 22% and 30%. Concrete machinery saw the strongest growth, slightly above the levels seen in the other sectors. From a regional perspective, the markets that were hit hardest in 2020 – particularly the UK and Spain – saw the best performances in 2021. Southern Europe and CEE markets saw above-average growth in sales, and even the mature markets in Northern Europe saw similar levels of recovery. None of the markets saw a fall in sales in 2021, and the only market that experienced single-digit growth was the high-volume German market. The fact that it has still not reached saturation levels can be considered a positive outcome. Turkey continued its recovery from the catastrophic levels of decline seen in 2018/19 and saw the highest levels of growth across the market regions.

The business climate index for the industry recorded its highest ever value in the July 2021 survey and maintained extremely high levels throughout the rest of the year. In the first two months of 2022, there was another small improvement both for the current business situation and future sales expectations.

European manufacturers hope that supply-side bottlenecks will create less concerns for the rest of the year. The demand-side clearly remains strong, as all equipment sub-sectors were expecting business to improve in the months leading up to the summer of 2022. In February this year, the CECE Business Barometer, highlighted that more than 50% of manufacturers surveyed were experiencing order backlogs of six months or more. All statistics and surveys presented in the current Annual Economic Report have so far indicated that the European construction machinery industry is very well positioned. These expectations are likely to be negatively affected by the current tensions and the effects of the war in Ukraine, which cannot be estimated yet.