Retrospective: Cement industry development

US National Register of Historic Places

US National Register of Historic Places

wikipedia.org

wikipedia.org

cementkilns.co.uk

cementkilns.co.uk

Luis Fuentes

Luis Fuentes

AGICO

AGICO

OneStone Consulting

OneStone Consulting

KHD Humboldt Wedag

KHD Humboldt Wedag

USGS

USGS

Holcim

Holcim

OneStone Research

OneStone Research

OneStone Research

OneStone Research

OneStone Research

OneStone Research

OneStone Research

OneStone Research

OneStone Research

OneStone Research

CEMBUREAU

CEMBUREAU

CEMBUREAU

CEMBUREAU

The history of the cement industry is full of inventions and interesting facts. In this article we will look back at how industrial cement production began and how it developed to the industry known today. We look back to main technology innovations such as the rotary kiln and calciner, the global cement demand development, international expansion and the challenges the cement industry faces today.

1 Introduction

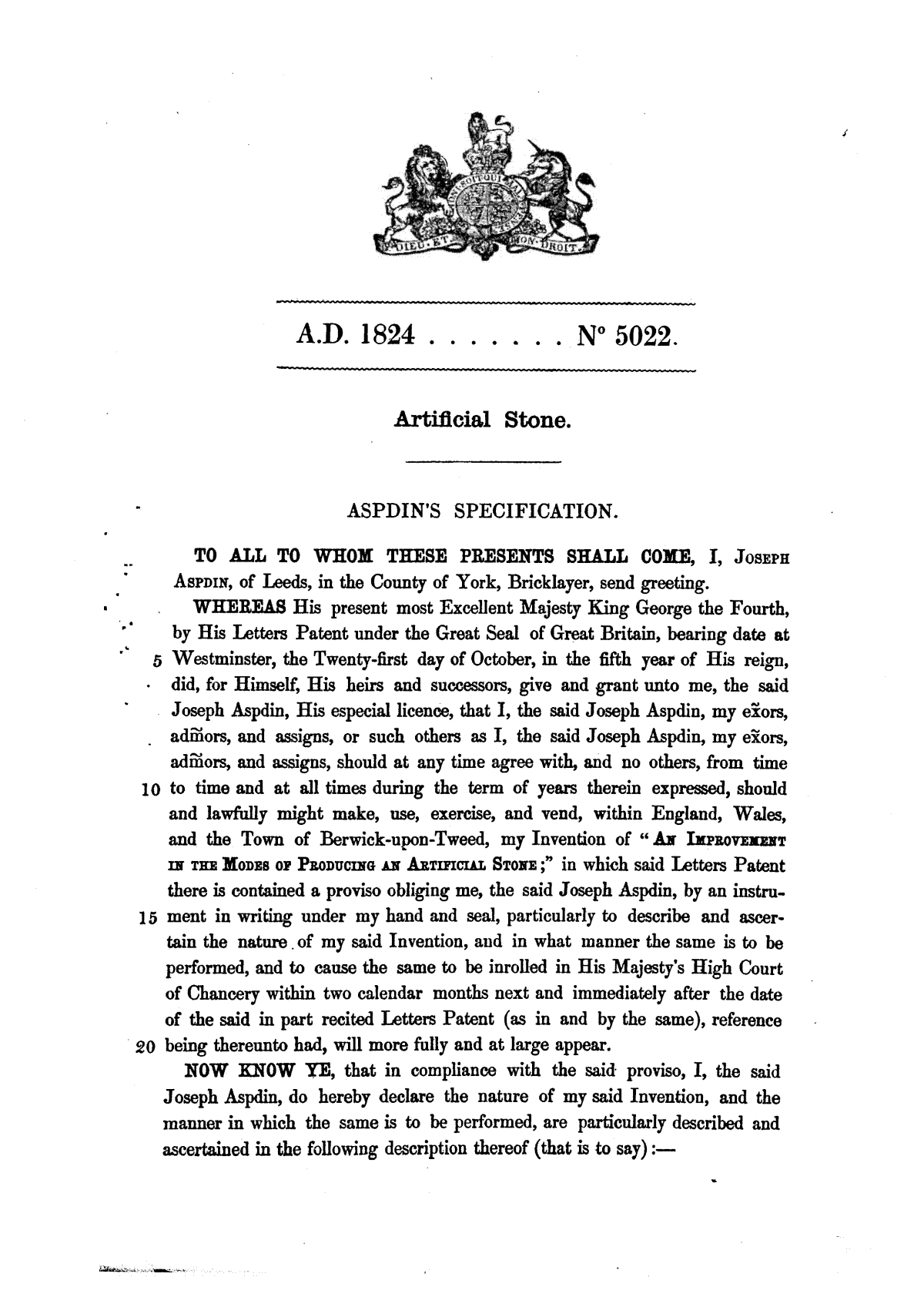

Who invented it? Today, the answer is that in 1824 Joseph Aspdin from Leeds in England obtained the patent for Portland Cement after he experimented with heating limestone and clay until the mixture calcined and then mixing the ground product with water to form an artificial stone (Figure 1). Aspdin named the calcined product ‘Portland Cement’, after the natural stone from the Isle of Portland in the English Channel. Portland Cement and any other modern cements are hydraulic cements that undergo hydration to cure and harden into a desired form. Hydraulic cements are sometimes also referred to as being ‘water resistant’, because they can cure in wet or submerged environments. Non-hydraulic cements, on the other hand, harden through a reaction with CO2 in the atmosphere, but are unable to cure and harden when exposed to water. These types of product are often referred to as mortars and were discovered as far back as 2000 BC in Central India and prehistoric Greece.

The origin of hydraulic cements goes back to around 800 BC, when the Phoenicians already had the knowledge that a mixture of burnt lime and volcanic ash could be used to produce hydraulic lime, that was not only stronger than any artificial stone previously used, but also hardened under water. Later the Greeks and Romans also used the knowledge of hydraulic cement production by using burnt lime and volcanic ashes, or a mixture of burnt lime and crushed tiles and bricks composed of burned clay. The Romans used the burnt clay-lime mix as their first hydraulic cement to line water-infrastructure buildings such as aqueducts for transporting water over long distances to their cities. The burnt clay provided similar cementitious properties to the so-called pozzolans, volcanic ashes or pitsands which were taken e.g. from the village of Pozzuoli close to the Vesuvius volcano in Italy or volcanic tuff, which was taken from the Island of Thera in Greece.

2 Industrial cement manufacturing

2.1 The beginnings

In 1843, the first cement plant making Portland Cement was the one of William Aspdin, the son of Joseph Apsdin, in Rotherhithe in London. The plant was operational from 1843 to 1846 and produced approximately 7000 t of cement clinker in that time. He modified his father’s cement formulation by increasing the limestone content in the mixture and burning it much harder. Isaac Charles Johnson, who was a competitor to Aspdin, succeeded in manufacturing a similar cement clinker for J. B. White & Co.’s nearby Swanscombe plant. Aspdin moved his operations to Northfleet, where three wet process bottle kilns were built with a production capacity of about 10 t/d. Several more plants were built in the United Kingdom. Aspdin sold out his share of the Northfleet plant in 1852, and set up a number of new cement companies, while the Northfleet plant continued making Portland cement on a small scale as Robins & Co. Ltd. until it was taken over by APCM (Blue Circle) in 1900.

Aspdin moved to Germany and in 1862, together with Edward Fewer, established a cement plant in Lägerdorf (Northern Germany, at that time part of the Kingdom of Denmark), which was then taken over in 1864 by Fewer to operate four shaft kilns, and what has been named ‘Englische Fabrik’. Another entrepreneur was Gustav Ludwig Alsen, who also built a cement plant in Itzehoe, close to Lägerdorf. In 1866, this plant already operated eight shaft kilns and in 1898 acquired the Fewer cement works. Alsen, after further expansion to Alsen-Breitenburg Zementwerke, merged with Nordzement more than a hundred years later and became Holcim Germany in 2003. However, in the year 1850 the first Portland cement plant in Germany was built in Buxtehude, Southwest of Hamburg. In 1863, a first Portland Cement plant was built in Nieder-Ingelheim in Southern Germany by Carl Krebs and later acquired by Heidelberger Zement. Only in 1872 was the first cement plant built in the area of Beckum in Western Germany, which later became one of the centres of the German cement industry.

In France, the first Vicat cement factory was built in 1853 by Joseph Vicat in Le Genevrey-de-Vif in the Isere region. The move to the cement industry was inspired by the invention of his father Louis Vicat, who already in 1817 published an article in the scientific journal ‘Les Annales de Chimie’ in which he presented his discoveries about the hydraulic phenomena of lime and cement, with the ability of burnt lime to set under water. In Italy, the first hydraulic cement that showed extraordinary properties for those times, was produced in 1864 in the Scanzo cement plant, near Bergamo, by the Bergamo Cement and Hydraulic Lime Co. (acquired by the Pesenti family, who owned Italcementi). In the USA, the first Portland cement was produced in 1875

in Coplay, Lehigh County, Pennsylvania, by the Coplay Cement Company plant under the direction of David O. Saylor, also known as the ‘father of the American cement industry’. India entered Portland Cement Production in 1914, when the Indian Cement Company Ltd. started manufacturing cement in Porbundar in Gu-jarat.

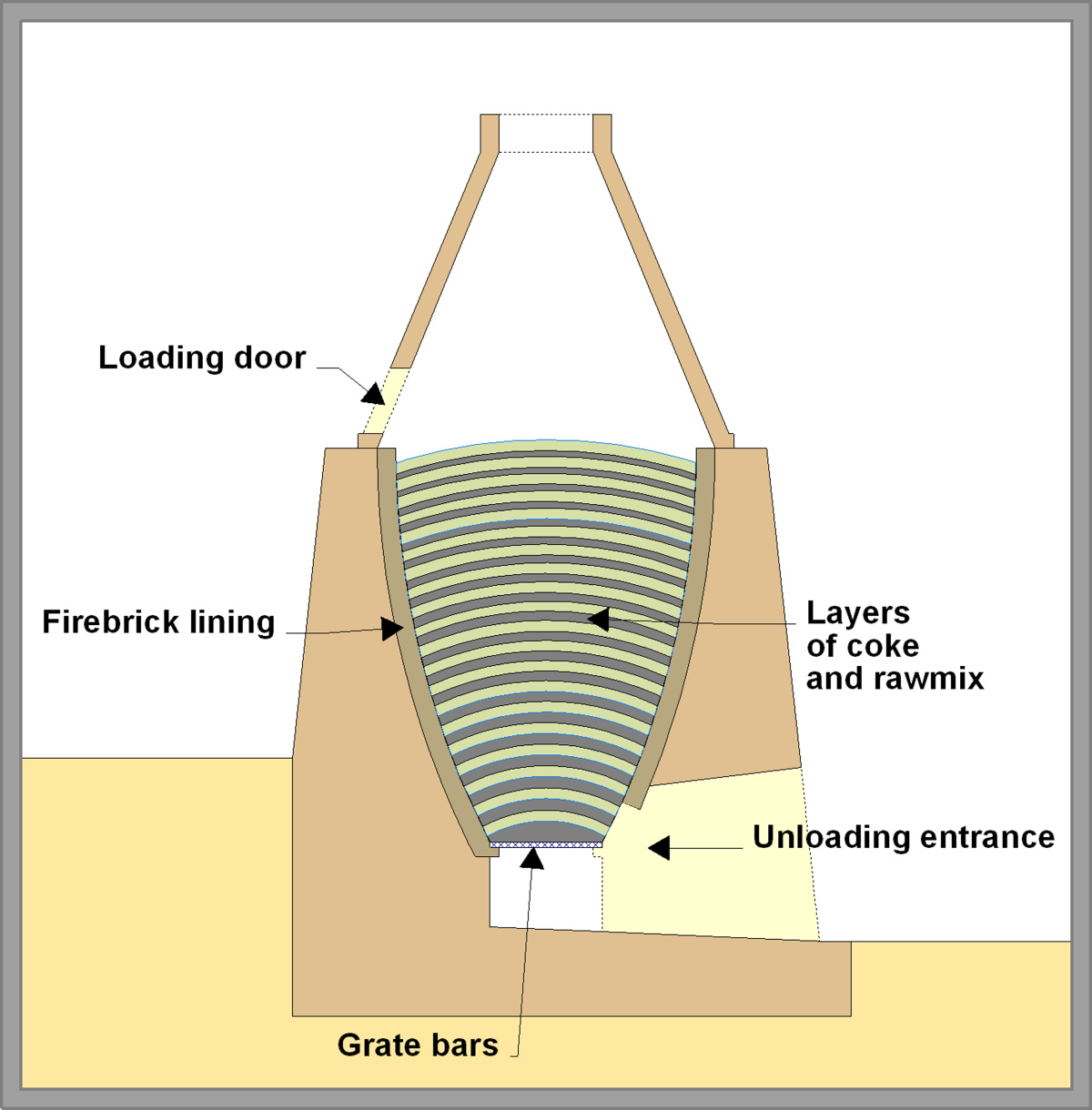

The kilns that were used for the first Portland cement plants were so-called bottle kilns (Figure 2), which were similar to the lime kilns that were used in the Mid-19th century. The kilns were hemi-spheroidal (i.e. egg-cup shaped), with diameters typically between 10-18 feet, and a depth some-what greater than the diameter. The raw material mix in lump form was placed into the kiln in domed layers. In order to avoid collapse of the charge, the layers needed to maintain their shape throughout the burning process. Loading and emptying of the kiln were each accomplished in a 12-hour day shift. Cooling took 1-2 extra days. A ten-foot kiln produced around 10 t of clinker per charge, while an eighteen-foot kiln produced 30 t, in a roughly linear relationship. However, the kilns were not efficient and produced a low cement clinker quality. In 1885, the estimated worldwide number of bottle kilns peaked with about 850 units, which had a combined clinker capacity of 1.1 million annual t (Mt/a).

2.2 Invention of the rotary cement kilns

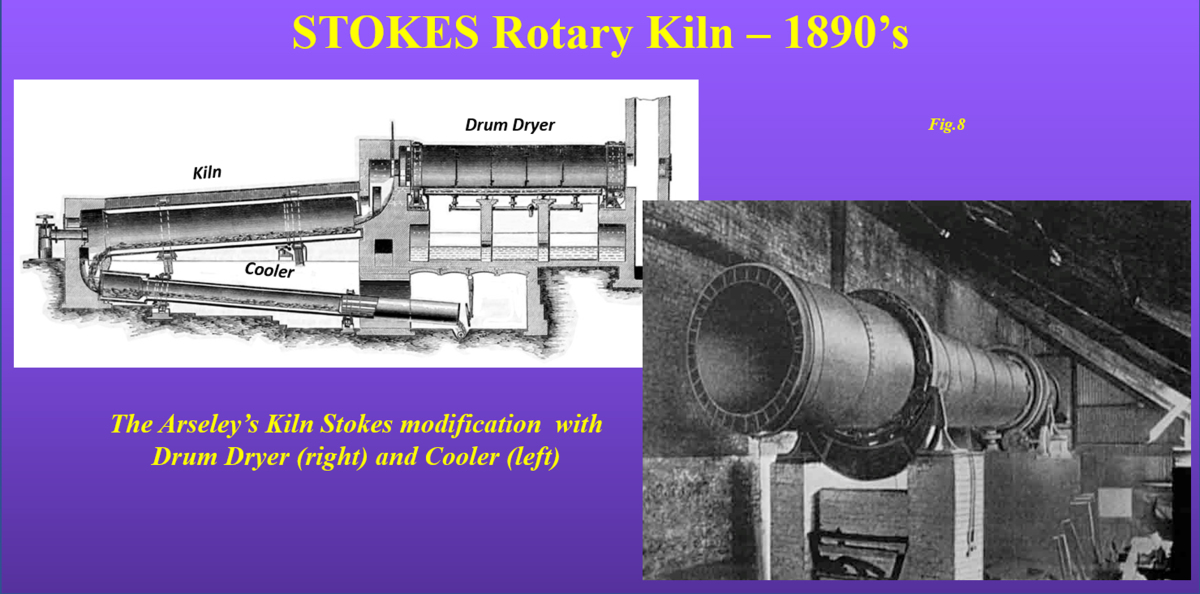

The invention of the rotary kiln was a key step in the history of the cement industry. The first rotary kiln patent was awarded in 1877 to Thomas Russell Crampton from England for a slightly-sloping rotating cylinder with firebrick lining and fuel burned in a single large flame at the lower end. The concept was further developed in 1885 by Frederick Ransome, who specified gas as a fuel and that the raw mix should be finely ground. The next invention was in 1888 by Frederick Wilfrid Scott Stokes, who extended the rotary kiln by adding a drum dryer and rotary cooler (Figure 3). However, the first operational rotary kilns mostly failed, because of a very short life of the firebrick linings, high heat losses, insufficient clinkering temperatures and frequent blockages because of ball and ring formation within the kiln. Engineer Jose F. de Navarro bought in 1889 the US rights for the Ransome kiln and was much more successful with the performance in a first installation at Keystone Portland Cement at Coplay, Pennsylvania, after experimentation with the raw mix powder, solving the lining problem and using oil instead of gas.

By 1895 several American manufacturers, incl. Lathbury and Spackmann, established the layout of the rotary cement kiln. The first successful kilns were about 1.5 m in diameter and 15 m in length. On a continuous operating basis, such a kiln made 20 t/d of clinker. After 1895 the fuel economy was improved by replacing oil with pulverized coal. By 1905 the largest kilns were 2.7 m in diameter and 60 m in length, making more than 150 t/d of clinker. The innovation was so spectacular that the USA cement production increased from 2.7 Mt/a in 1900 to 8.9 Mt/a in 1907, corresponding to about half of the global cement production in that year. FLSmidth and Polysius (thyssenkrupp) were among the companies who visited the USA to obtain information about the technology. Polysius manufactured and supplied its first rotary kiln in 1889 and established themselves as a cement plant turnkey supplier in 1907. FLSmidth sold its first rotary kilns in 1899, and by 1921 the company had sold about 300 rotary kilns worldwide.

The first rotary kilns were either wet or semi-wet, because the raw mix was fed to the kiln as a slurry. For raw material preparation wet grinding mills (ball mills) could be used, having a better efficiency than dry ball mills. However, the wet process suffered from the disadvantage that a large extra amount of fuel is used for evaporating the water and that larger kilns were needed for higher throughputs (Figure 4). So for producing 3000 t/d of clinker, kilns up to 6.0 x 225 m in size were being used. With the development of clinker manufacturing and the preheating of the dry raw materials, first in Lepol kilns and later through the use of cyclone preheaters, the technology completely changed so that wet process kilns became inefficient and were substituted by dry processing. The situation was further influenced by the development of vertical roller mills (VRM), which were able to finely grind dry raw materials. Nowadays, with the latest dry processing technologies using a precalciner and cyclone preheaters, rotary kilns have sizes of 6.5 x 95 m to produce up to 12000 t/d.

2.3 Invention of the suspension preheater and precalciner

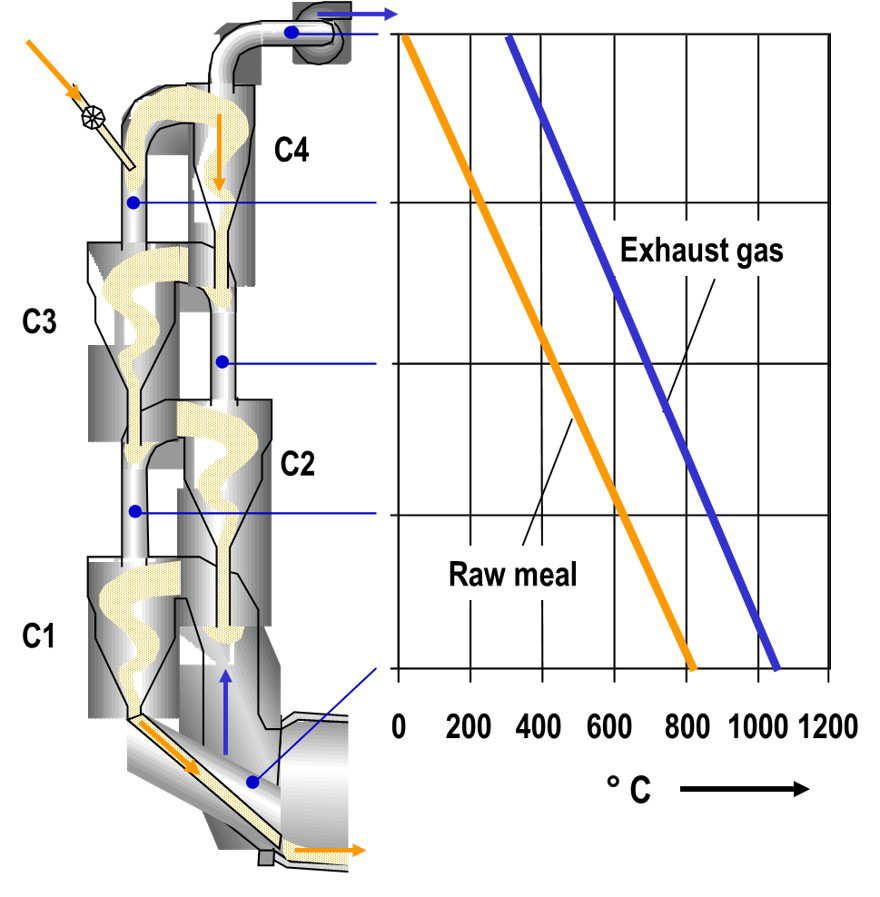

The decades from the 1950s to the 1980s were a time of constantly-increasing worldwide demand for cement, as well as stricter environmental regulations and an energy crisis in 1970. The requirements shifted to kiln systems with higher capacity, better thermal efficiency, stable operation, higher clinker quality and lower emissions. Accordingly, in these years first the SP kilns (SP = Suspension Preheater) and then the NSP kilns (New Suspension Preheater) were developed. In Germany at the end of the 1950s, KHD Humboldt Wedag built the first preheater kiln, which reduced the heat consumption for clinker production at that time by 50%. The concept of a multi-stage preheater is illustrated in Figure 5. The cement raw meal, in countercurrent to the kiln exit gas, is fed into the uppermost cyclone stage (C4) of a suspension preheater, heated up by the ambient gas temperature and separated into the lower cyclone stages. This process is repeated correspondingly with the higher temperatures until the raw meal leaves the lowest cyclone stage (C1) at about 820 °C to be fed into the rotary kiln [3].

Calcination, i.e. the decarbonation or decomposition of CaCO3 into CaO and CO2 in the presence of SiO2, Al2O3 and Fe2O3 begins already at 550 °C to 600 °C and proceeds very quickly above 900 °C. With a suspension preheater it is possible to achieve precalcination rates of 30 to 40%, depending on the kind of raw meal and possible temperatures. The residual calcination takes place in the rotary kiln. In 1965, KHD Humboldt Wedag equipped the kiln system of the Dotternhausen Cement works in Germany with an additional preheater burner to achieve a higher calcination outside the kiln. Accordingly, the NSP kiln with additional calciner was born. In 1973, Krupp Polysius obtained a first order from Ciments Lafarge to supply a Prepol-AT calciner with a specially designed combustion chamber for raw meal and fuel. From that time onwards, kiln systems with precalciner became the norm. Today, with modern calciners and grate coolers, which supply the necessary tertiary air, it is possible to achieve 90 to 95% of the calcination outside the rotary kiln. With this system, 50 to 65% of the fuel is burned in the precalciner and only 35 to 50% in the rotary kiln [1].

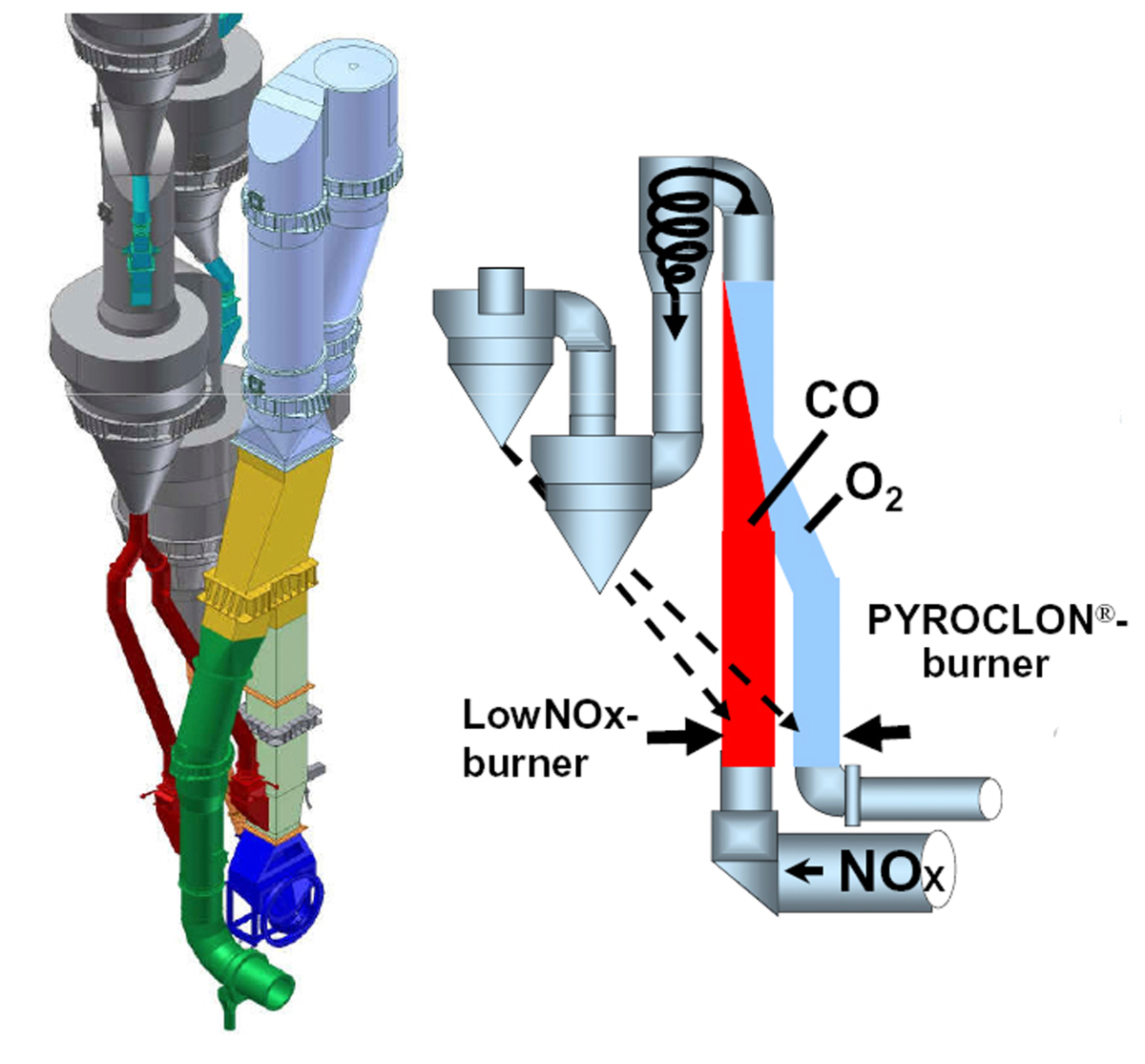

Precalciners can be designed for very special purposes. After the reduction of fuel consumption, the next development was the reduction of NOx emissions thanks to measures on the primary side in the preheater/kiln system and the use of alternative fuels. This development was already triggered in Japan in the early 1980s due to the country’s tightened environmental requirements. With the DD calciner, Kobelco and Nihon Cement launched a system with an adjustable nitrogen oxide reduction zone onto the market as early as 1979. In 1989, Krupp Polysius launched the MSC (Multi-Stage Combustion) process on the market. FLSmidth developed the ILC (Inline calciner) and SLS (Separate line calciner) systems with low NOx features and unique flexibility in fuel use. Modern calciners with NOx reduction zones and multi-stage combustion (Figure 6) can achieve emission levels of 500 to 800 mg NOx/Nm3 of exhaust gas. However, for lower emission levels selective non-catalytic reduction (SNCR) or selective catalytic reduction (SCR) are required [4].

3 World cement production

3.1 Cement demand

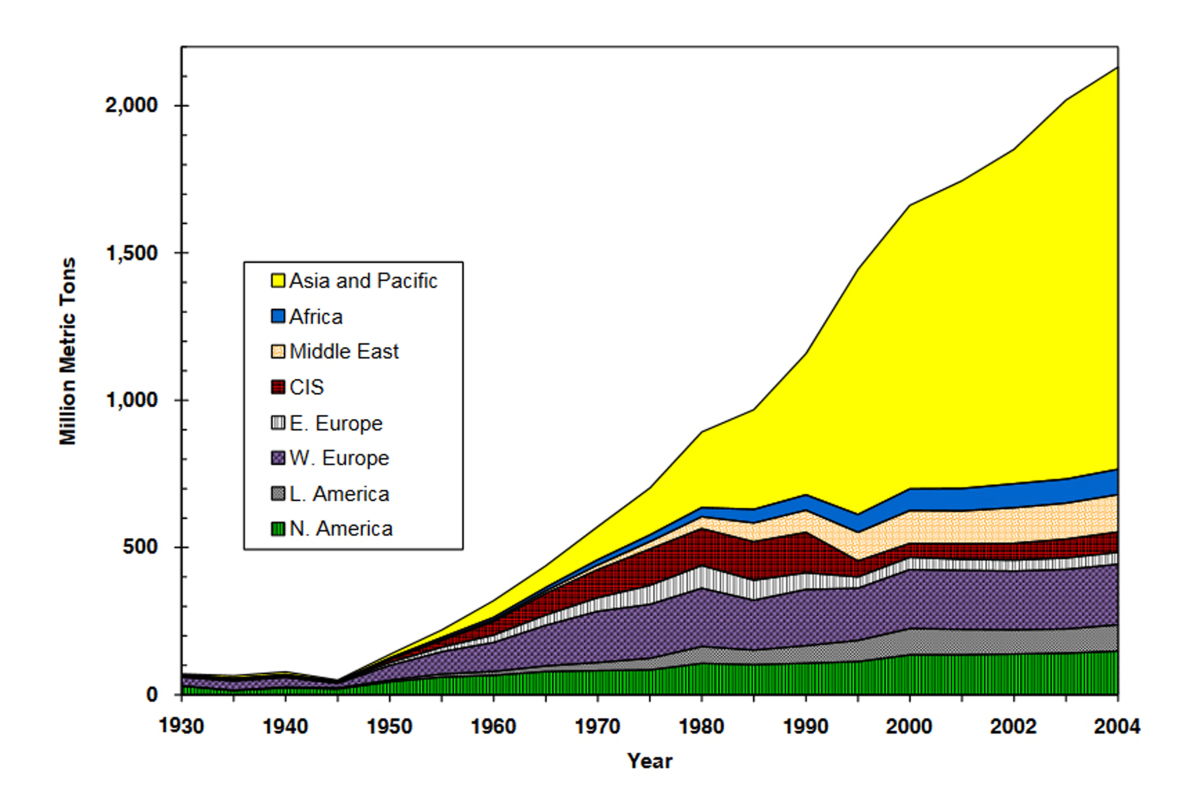

According to the USGS [5], the global hydraulic cement production increased from about 18 Mt/a in 1907 to almost 100 Mt/a by 1948. However, with the global construction boom, which started in 1950, cement production experienced a very strong growth to about 2195 Mt/a in 2004 (Figure 7) and 4105 Mt/a in 2020. The cement production capacity increased from about 25 Mt/a in 1907 to 6270 Mt/a in 2020. As can be seen in Figure 7, the largest growth in cement production has been in Asia, which currently accounts for 75.6% of global cement production. Much of Asia’s growth has been in China. In 1950, China produced only about 2 Mt/a of cement, whereas by 2020 this figure had increased to 2370 Mt/a or 57.7% of global cement production. The global cement and clinker trade peaked in 2019 at a level of 215 Mt/a. According to the Turkish Cement Producer Association, 95 Mt/a of the global trade were clinker exports.

While in 1907 the production of 18 Mt/a hydraulic Portland cements (which later was referred to as Ordinary Portland Cement or OPC) required about 17.1 Mt/a (95%) of clinker and 0.9 Mt/a (5%) gypsum, the clinker factor declined significantly since that time due to the introduction of blended cements. Beside clinker and gypsum, these cements use several other supplementary cementitious products (SCP), such as granulated blast furnace slag (GBFS), fly ash or natural pozzolans. In many countries, the share of OCP has fallen to less than 20% and the use of blended Portland cements and special cements has increased to more than 80%. With growing use of SCPs and the addition of ground limestone to blended cements the global clinker factor (clinker to cement ratio) has fallen below 75% today, and further reductions are envisaged. Accordingly, with growing cement demand and lower clinker factor the cement grinding capacity has increased quicker than the clinker capacity and new cement grinding mills such as VRM, roller presses (HPGR) and Horomills have been invented.

3.2 Internationalisation

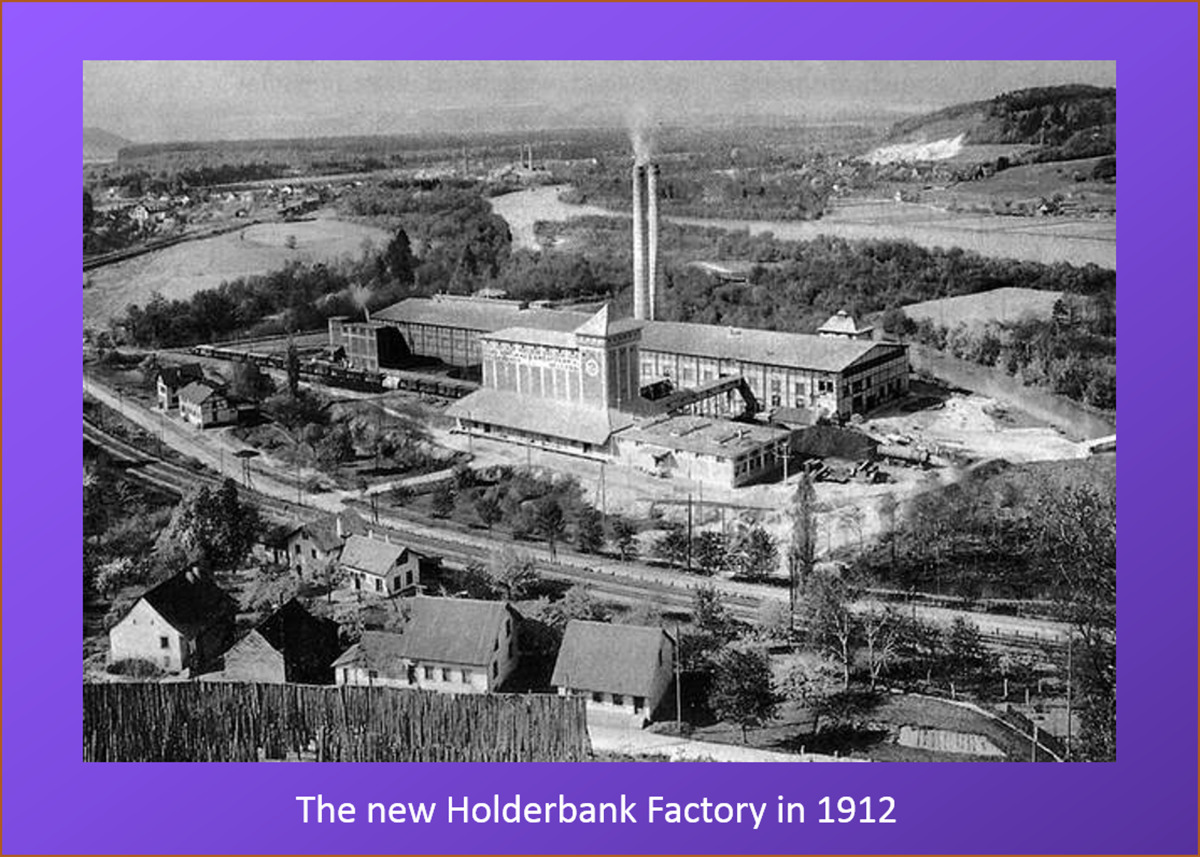

In the last century, the cement industry saw a huge internationalisation. The pioneers of the global expansion strategy were Holderbank (Holcim), Blue Circle, Lafarge, Ciments Francais, Heidelberg-Cement, Vicat, Italcementi, Cimpor, Cemex and Taiheiyo. Holderbank set up its first cement plant (Figure 8) in Switzerland in 1912 and has been one of the most active cement companies in international expansion, beginning in the 1920s. In 1923, Holderbank acquired Dutch Nederlandse Cement and in 1926 Ciments d’Obourg in Belgium was acquired. In 1927, Holderbank built the Ciments de Chalkis cement plants in Greece and in 1929 the Tourah cement plant in Egypt. Plants in Lebanon and South Africa soon followed. After 1952, Holderbank expanded to Canada, then throughout North and South America. In the late 1970s and early 1980s, the company continued its expansion in Latin America and also entered Spain, Eastern Europe and Asia for the first time. By 1986, Holderbank was the world’s largest cement manufacturer and changed its name to Holcim in 2001.

Nevertheless, the first overseas move was made by Blue Circle Cement, who were founded in 1900 in England as Associated Portland Cement. Their overseas activities began in 1912, when they bought the Tolteca cement plant in Mexico and two more plants in Canada and South Africa. From 1950 to 1970, Blue Circle became the largest cement manufacturer in the World with its own new plants in England and further acquisitions in Australia, New Zealand, Malaysia, Indonesia, The Philippines, India, Africa, South America and Europe. However, due to the 1970 Energy crisis and the worldwide contraction of the cement markets, major overseas investments were sold in the 1980s, and in 2001 Blue Circle was taken over by the French company Lafarge. Lafarge itself built a cement plant in Canada in 1956, formed Lafarge Cement North America and merged this company in 1970 with Canada Cement. 1973, Lafarge North America moved south to the USA to acquire Lone Star Industries and after the USA recession 1982, General Portland Cement, the second largest US cement producer was acquired. Lafarge merged with Holcim in 2014.

After several acquisitions in France, Lafarge’s French competitor Ciments Francais turned to international expansion during the 1970s in order to protect the company from the cyclical nature of the business in just one country. In 1976, the US Coplay Cement Company was acquired, followed by Louisville Cement and Lake Ontario Cement in Canada. In 1989, the company entered Turkey and Spain. Compagnie des Ciments Belges, San Juan Cement (U.S.A.), and Halyps (Greece) were acquired in 1990. Ciments Francais was taken over by Italcementi in 1992. Following this acquisition, Italcementi became active in international expansion. Since 1998, Italcementi further expanded through acquisitions of cement assets in Bulgaria, Kazakhstan, Thailand, Morocco, India, Eygpt and the United States. In 2015, Italcementi was taken over by HeidelbergCement.

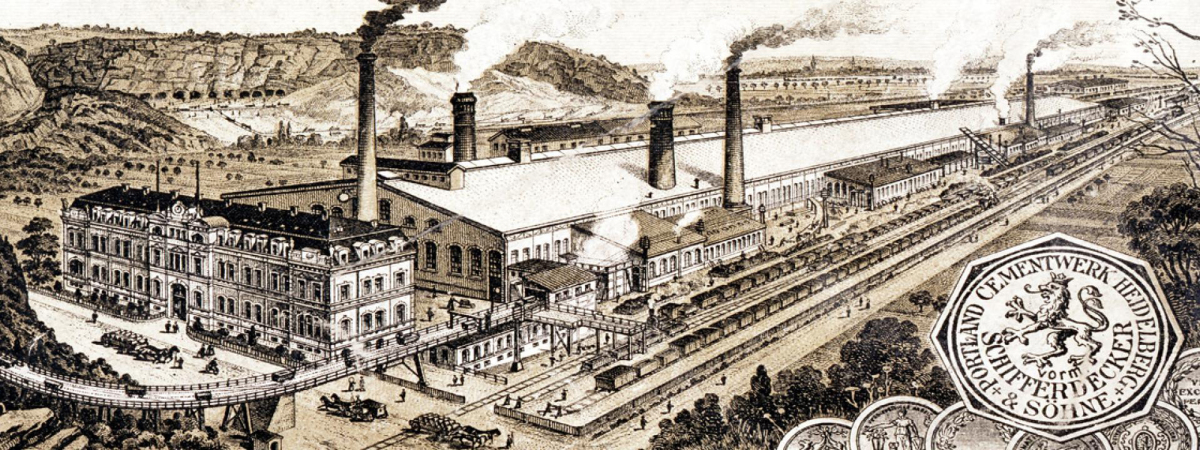

HeidelbergCement had its main cement works close the Heidelberg headquarters in Leimen (Figure 9), where production began in 1896. The company’s international expansion started with buying a stake in French cement producer Vicat in 1968. In 1977, a massive investment program in North America began with the acquisition of Lehigh Cement. In 1998, several investments and acquisitions were started in Central and Eastern Europe. In 1993, SA Cimenteries CBR in Belgium was acquired. In China, the company has been active with a JV in the Guangdong province since 1995. In Turkey, Akçansa, a joint venture of Sabanci Holding and HeidelbergCement, was founded in 1996. The history of HeidelbergCement in Africa dates back to its acquisition of Scancem in 1999. Scancem’s Sub-Saharan African business even dates back to the mid-1960s, when excess clinker capacity from their Scandinavian plants was sold to African countries and the first separate cement grinding plants were installed or acquired in Benin, Ghana, Liberia and Togo. In 2007, Heidelberg-Cement divested its 35% share in Vicat.

Vicat made its first foreign acquisition through the purchase of National Cement in Ragland, USA, in 1974. This was complemented by the acquisition of the Lebec cement plant in California, in 1987. International expansion continued in the 2000s with acquisitions in Switzerland, Italy, Turkey, Kazakhstan, Egypt, Senegal, Mali, Mauritania, India, and Brazil. Taiheiyo started its foreign expansion in 1989 with Dalian-Onoda Cement in China. In 1990, the US-based California Portland Cement was acquired and in 1995 Nghi Son Cement in Vietnam was established. Cemex began its internationalisation in 1992 with acquisitions in Spain. In 1995 and 1996, cement companies in the Dominican Republic and Colombia were acquired. From 1997 to 1999 the company expanded to Asia and Africa with major purchases in the Philippines, Indonesia and Egypt. US Southdown Cement followed in 2000. Cimpor started its foreign expansions with the acquisition of Spain’s Corporation Noroeste in 1992, Cimentos de Mozambique in 1994 and Asment Temara in Morocco in 1996. In 1997 two cement companies in Brazil were acquired.

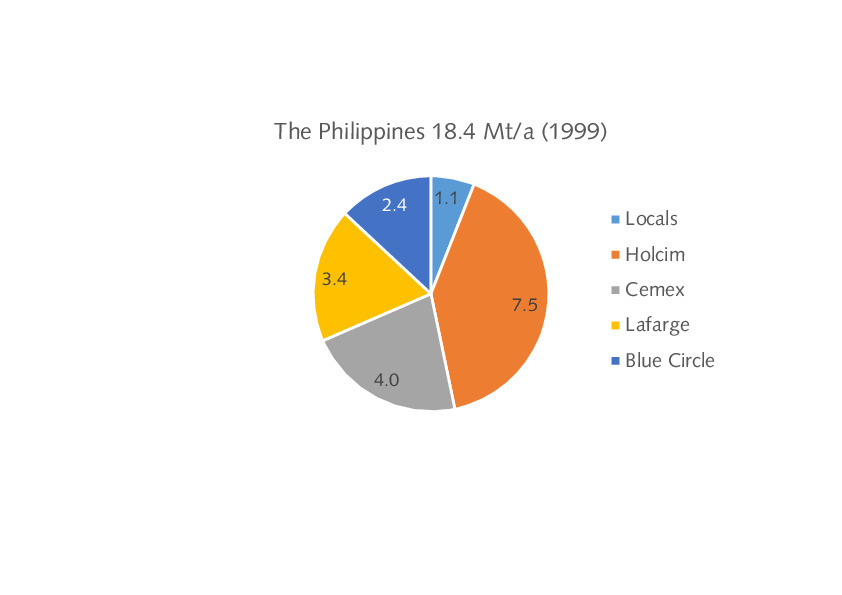

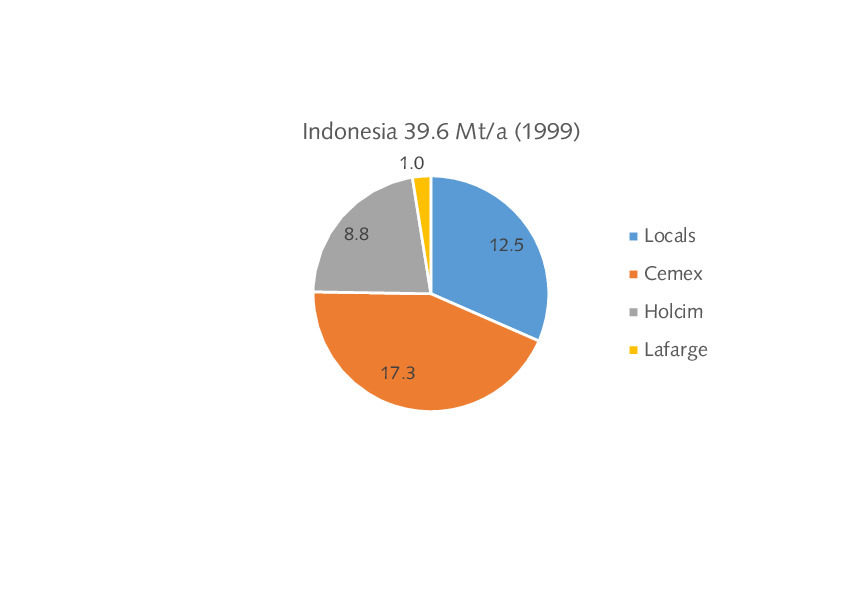

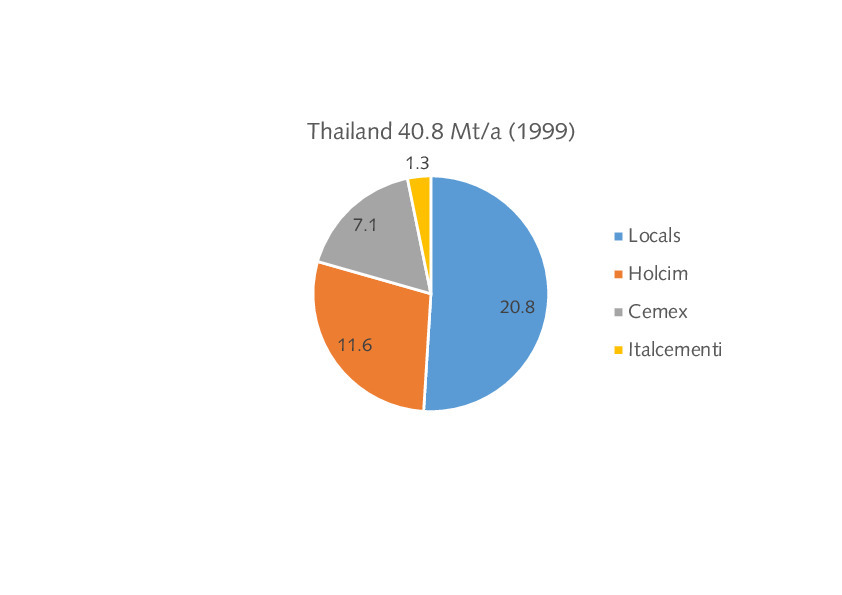

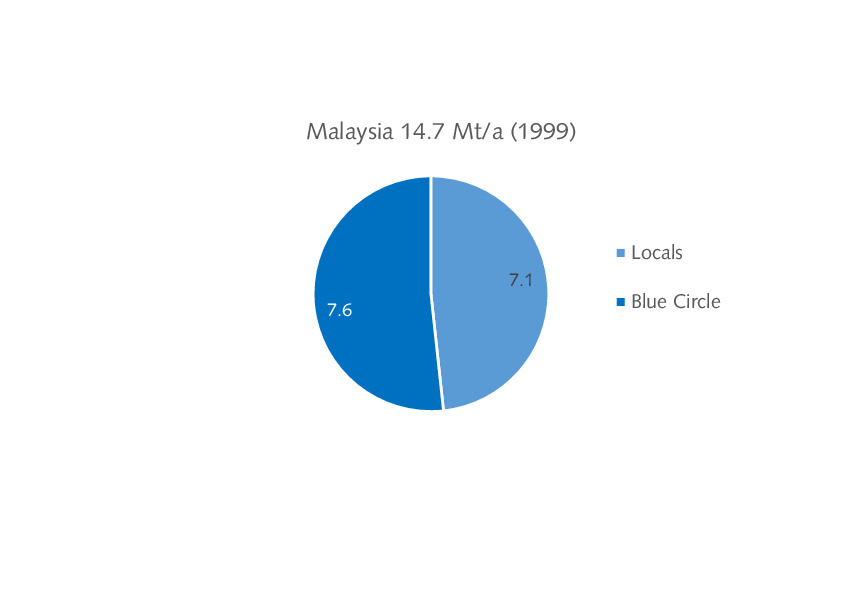

However, probably the largest acquisition rush by Western cement companies took place in East Asia after the currency crisis of 1997, when local cement companies were faced with over-production and unpayable debts. Mostly affected were cement producers in the SE Asian countries of Thailand, Indonesia, The Philippines and Malaysia, where the foreign share dramatically changed by July 1999 (Figures 10-13). In the Philippines, Holderbank, Cemex, Lafarge and Blue Circle took over 94% of the cement production capacity. In Indonesia, Cemex, Holderbank and Lafarge obtained 68%. In Malaysia, Blue Circle obtained 52% and in Thailand Holderbank, Cemex and Italcementi were able to obtain 49% of the capacity. HeidelbergCement stepped in later and has been the majority shareholder of Indocement in Indonesia since 2001.

4 Today’s challenges

The investment needed to build an integrated cement plant with combined clinker and cement production is between US$ 100 and 170 million per Mt/a capacity, depending on the owner’s preferences, location and how stringent and complex the environmental regulations and authorization processes are. High capital and technical barriers to entering the sector, together with relatively high maintenance costs and technological upgrades, place cement manufacturing among the most capital-intensive industries. However, this can get even more complex and difficult when the cement industry is forced to significantly reduce its CO2 footprint [6]. The cement producers in Western Europe are leading in this sector. By 2050, the objective is to implement the concept of carbon neutrality of the cement and concrete industry, which is backed by most of the major cement producers and global cement institutions. This goal can only be achieved if carbon capture, utilisation and storage (CCUS) concepts are implemented.

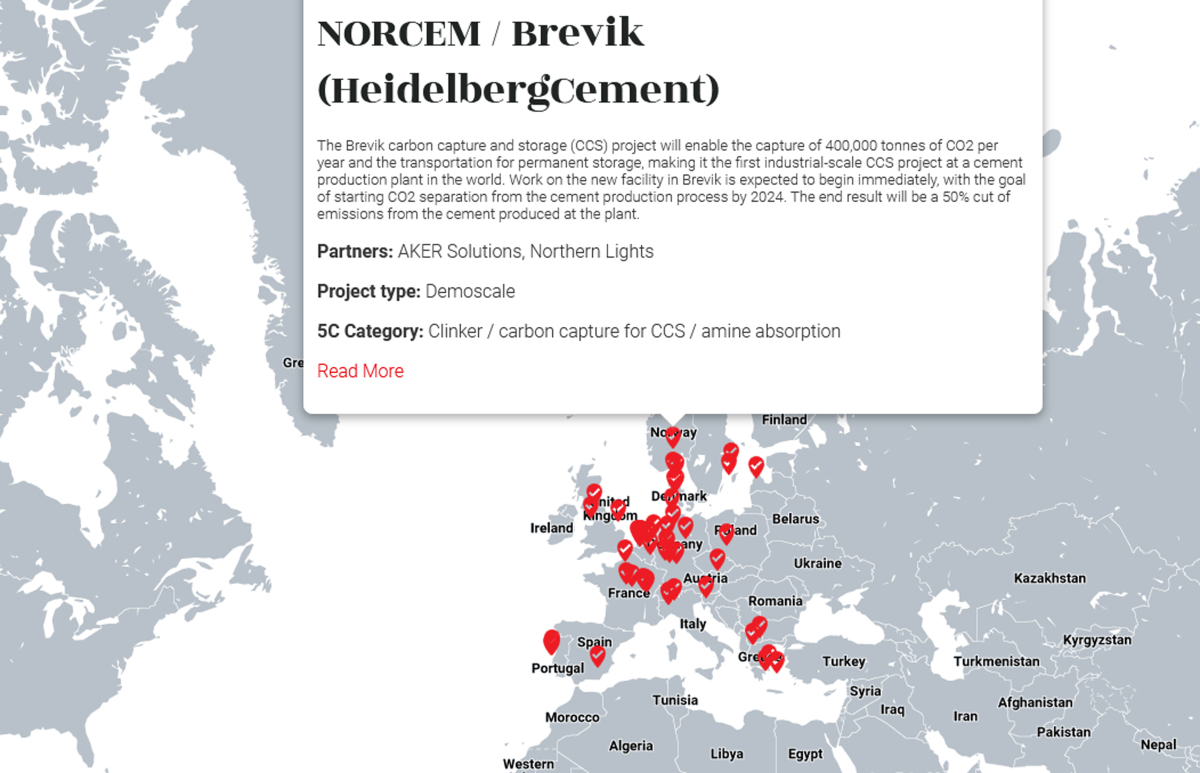

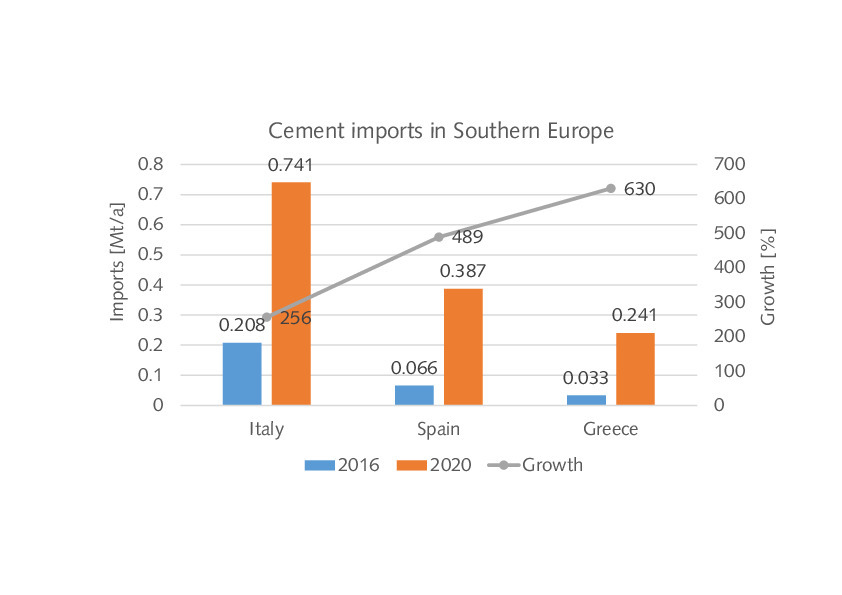

Cembureau, the European Cement Association, published an interactive map (Figure 14), which is available on their website and currently identifies a total of 53 decarbonisation projects by the European cement industry across Europe. The projects involve different technologies, including CCUS, the phase out of fossil fuels and their replacement with alternative fuels and biomass waste, the development of low clinker cements, the recarbonation of concrete and the mineralization of aggregates. Calculations were made that ETS prices (ETS = EU Emission Trading Scheme) of € 90/t CO2 will increase the prices in the EU for cement at a clinker ratio of 74% by 7.23 €/t, or 12-15% of the cement production costs when the free allocations fall by 2026. The result could be even higher cement imports to the EU and additional plant closures. According to Eurostat, cement imports (Figure 15) already increased massively in the Mediterranean countries from 2016 to 2020.