Cement industry challenges in the new decade

CRH

CRH

OneStone Consulting

OneStone Consulting

OneStone Consulting

OneStone Consulting

OneStone Consulting

OneStone Consulting

OneStone Consulting

OneStone Consulting

OneStone Consulting

OneStone Consulting

OneStone Consulting

OneStone Consulting

OneStone Consulting

OneStone Consulting

USGS

USGS

OneStone Research

OneStone Research

LafargeHolcim

LafargeHolcim

OneStone Research

OneStone Research

OneStone Research

OneStone Research

Dangote Cement

Dangote Cement

HeidelbergCement

HeidelbergCement

OYAK Group

OYAK Group

Eurocement Holding

Eurocement Holding

HeidelbergCement

HeidelbergCement

The cement industry faces a number of challenges. One major challenge is the impact of the Covid-19 pandemic, which led to a decline in demand for cement and all other business lines such as ready-mixed concrete (RMX), aggregates and asphalt. In this article the latest market development is outlined with a review of selected countries and cement producers and how industry profitability has changed. Another challenge is the reduction of CO2 emissions, because the cement industry contributes 6 to 8% of global carbon emissions. Here, the latest achievements and targets are outlined and how the re-carbonation concept will contribute in future.

1 Introduction

The cement industry has a large impact on the global economy due to its long and diverse supply chain comprising mining of the raw materials and the use of cement in the concrete industry. According to the International Finance Corporation (IFC) the cement sector contributes 5.4% of the global gross domestic product and 7.7% of the world’s employment [1]. Cement/concrete is the second-most utilized product in the world after potable water. The material is used to build houses, bridges, roads, airports and harbours. Large dams supply us with water, concrete pipes distribute the water to households. Cement and concrete help to construct hospitals, schools and kindergartens, which contribute to the health, education and well-being of society.

However, today the cement industry contributes 6 to 8% of global carbon emissions. Globally, cement is produced in 162 countries by more than 1000 producers in about 3000 cement plants, of which about 75% are integrated plants (clinker and cement production) and 25% are grinding plants (cement production only). In the last few years, the growth in new cement capacities has exceeded the growth in cement production, despite the capital intensity of the industry. The Covid-19 pandemic has slowed construction in many countries and accordingly, the demand for cement has further decreased. The profitability of many cement companies has declined and the balance sheet and liquidity of listed cement producers does not allow for significant new investments.

2 The Covid-19 impact

OneStone Consulting published a market report in May last year with the title “Covid-19 Impact Analysis on the Global Cement Production” [2]. This report at the beginning of the pandemic provided latest market information about the impact of the on-going coronavirus pandemic on global cement production, with forecasts for 2020, 2021 and 2025. It draws on data taken from 75 countries that jointly represent almost 97% of all global cement capacity in 2019. For 2020 it was projected that the global cement production would decline by -9.3%, with a large decline in the 1st half and a gradual recovery in the 2nd half of the year. India was expected to be one of the countries with the largest decline by -14.2% in calendar year 2020. It was also expected that there would be large regional differences even in the European countries.

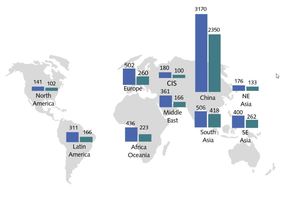

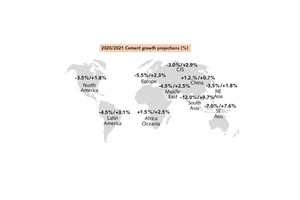

Globally, in 2019 about 4181 million t (Mt/a) of cement were produced. The worldwide cement capacity was 6180 Mt/a, which leads to an average cement capacity utilisation of 67.6% (Figure 1). The highest capacity utilisation rates were in South Asia with 82.7%, NE Asia with 75.7% and China with 74.1%, while the lowest utilisation rates were in the Middle East with 46.0%, Africa/Oceania with 51.1% and Europe (incl. Turkey) with 51.8%. Because of the capacity additions in recent years, countries formerly importing cement have switched to exports and the pressure on global cement exports has therefore increased. Due to the Covid-19 pandemic, the situation has further worsened. Figure 2 shows the latest forecast (Oct. 2020) for the regional cement production in 2020 and 2021. Globally, against all former projections, the cement production will decline in 2020 only by -1.8% (-5.6% excl. China), with a recovery in 2021 of +2.4% (+4.6% excl. China).

2.1 Situation in selected countries

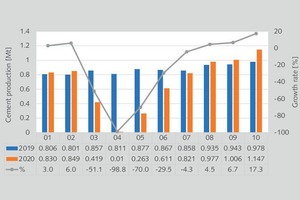

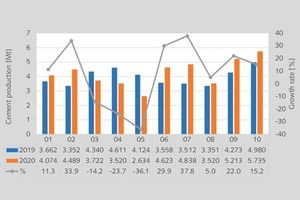

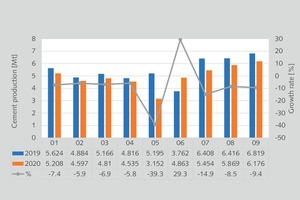

Peru is one of the countries in Latin America which was more severely hit by Covid-19 than others. At the beginning of December 2020 there were almost 1 million detected coronavirus cases and the death toll rose to more than 36000. Figure 3 shows Peru’s monthly cement production up to October 2020 compared with 2019. It is a typical V-shape curve, which was also projected for most of the other cement producing countries. In April the production came down nearly to zero. The months March, May and June were also very bad, but since August the production has recovered with positive growth rates. Anyhow, up to October the cement production in 2020 was still -20.6% behind 2019. Figure 4 shows the cement production development for Pakistan. Here a decline also started in March and continued until May. But since then, there has been a huge recovery with the accumulated production +6.6% yoy in October.

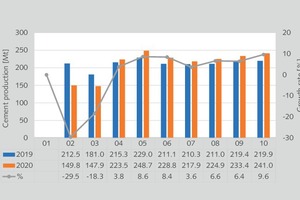

It is interesting how different the situation is in some of the most populous countries which were severely hit by Covid-19. But let us first start with China. What we know today is that the coronavirus outbreak started in China, but China managed to bring the pandemic under control. Figure 5 shows China’s monthly cement production until October 2020 compared with 2019. The cement production in February and March was massively impacted by the local lockdown, and after a recovery the accumulated production in May was still 8.1% behind 2019. However, by October the accumulated production was 0.3% higher than in 2019. For 2020 a 1.2% higher production than in 2019 is projected.

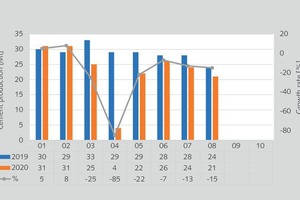

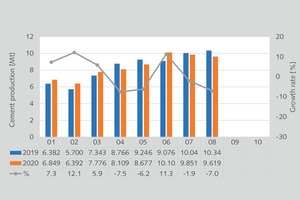

India had about 9.5 million Covid-19 cases at the beginning of December and a death toll of almost 140 thousand, but the daily cases have been in decline since September. The monthly cement production declined significantly in March, April and May 2020 (Figure 6). By August 2020 the accumulated production was -20.0% below the 2019 figures. For the rest of the year a slight recovery is projected, but 2020 will see a yoy decline by about 14-15%. Indonesia, which had about 540 thousand Covid-19 cases at the beginning of December and a death toll of about 17 thousand had a 9.0% yoy decline in the accumulated cement production by September 2020 (Figure 7). For the full year a decline by about 10% is projected because of a second wave of the coronavirus since November.

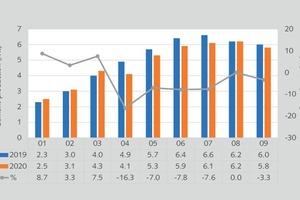

Up to now, the USA is the country hardest hit by the Covid-19 pandemic with almost 14 million cases at the beginning of December 2020 and a death toll of nearly 275 thousand. The country has been severely hit by a second wave which started at the end of October. However, up to now the monthly cement production has not been greatly influenced by the pandemic (Figure 8). On the contrary, due to significant cement production increases in the 1st Q 2020, the accumulated cement production at the end of August was still +0.7% above the 2019 figures. By the end of 2020 a yoy decline by 4.5% is projected. Russia had the 4th highest number of Covid-19 cases with about 2.3 million at the beginning of December and ranked in 10th place concerning the death toll. The cement production (Figure 9) was massively hit in April 2020, but since August there has been a slight recovery and the accumulated cement production in September only showed a -4.0% yoy decline.

2.2 Situation with selected cement producers

For most cement producers, the Covid-19 impact led to a decline in demand for cement and all other business lines such as ready-mixed concrete (RMX), aggregates and asphalt.

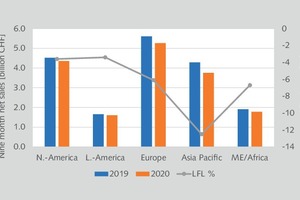

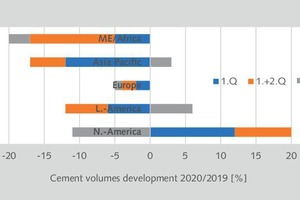

The LafargeHolcim Group is the largest cement producer outside China, with a cement production capacity of 287.0 Mt/a. As shown in Figure 10, in the first 9 months of 2020 the net turnover (LFL) of the Group to external parties, incl. contribution from JVs such as Huaxin in China, decreased from CHF 17.984 billion to CHF 16.759 billion, which is a decline by 6.8%. Figure 11 shows the quarterly cement volume development in the Group’s 5 world areas. The largest change from Q1 to Q3 is in North America with +12% and -11% respectively. Europe shows a relatively small impact. Latin America, Asia Pacific and the Middle East/Africa were severely impacted. However, beside North America all other regions had a significant Q3 recovery, which also leads to an optimistic projection for the 2020 results.

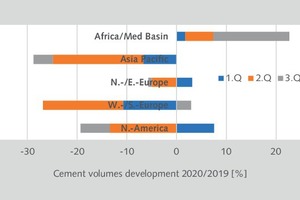

The revenue of HeidelbergCement Group (HC Group) decreased in the first nine months of 2020 by -7% (LFL) to € 13.140 billion, while the operating EBITDA increased by +6% (LFL) to € 2.731 billion. At the same time the cement sales volumes (incl. Group services) decreased by -4.0% to 90.112 Mt/a (LFL) while the sales volumes for aggregates decreased by -4.6%, the RMX volumes decreased by -9.5% and the asphalt volumes by -5.0%. Figure 12 shows how the quarterly cement volumes developed in different HC Group regions. In Q2 of 2020 the sales volumes suffered most in all the regions except Africa/Med. Basin. Q3 saw a significant recovery with the exception of North America. All in all, the cement volumes only decreased by -4.0% (LFL), which allows some optimism for Q4 and the complete year 2020.

Cemex, which is another TOP cement producer, also suffered from the Covid-19 impact but is looking optimistically into the future. Their cement volumes increased in the first 9 months of 2020 in Mexico by +2% and in the USA by +6% and still by +1% in Europe, when compared to the first 9 months of 2019. In some other countries there was a massive decline in the volumes, such as in Panama (-60%), Colombia (-20%), Costa Rica (-13%) and the Philippines (-12%). Despite the higher cement volumes, the RMX volumes declined in this period in Mexico by -20% and in Europe by -10%. Panama shows the highest decline in the RMX volumes with -74% yoy. Up to September the net sales decreased only by -2% (LFL) and accordingly Cemex is optimistic for Q4 and the annual 2020 results.

Within the other TOP global cement producers there are winners and underperformers in the development of cement volumes and corresponding company results up to September. Dangote Cement was able to increase its cement sales volumes in Nigeria (Figure 13) by 10.2% and in all African countries by +6.6% to 19.206 Mt/a in the first nine months, while revenues increased by +12.0% and EBITDA by +17.1%. Votorantim Cimentos recorded a +23% increase in net revenues in the first 9 months of 2020 (yoy), due to a +15% increase in sales in Q3 of 2020, resulting from a recovery in demand in all of the company’s regions. The cement sales at CRH declined by -7% (LFL) in the first nine months of 2020 yoy, while the EBITDA decreased in this period by -14% (LFL). Cement volumes were mainly increased in Brazil, Romania, Spain and Germany, while volume losses of more than -5% occurred in France, Switzerland and the UK.

India’s Ultratech Cement, having 114.8 Mt/a cement capacity after the acquisition of Century Cement in October 2019, suffered a decline in the first 9 calendar months of 2020 by -14.6% to 53.67 Mt/a in their cement volumes, after restated consolidated 62.81 Mt/a in the first 9 months of 2019. The largest decline with -31.9% was in Q2 of 2020 (Q1 of FY 2021), due to the nationwide lockdown and the shutdown of operating activities under government directive. However, Q3 of 2020 (Q1 of FY 2021) showed a recovery of +8.1% in the cement volumes. ACC Limited, which is part of LafargeHolcim, had a decline by -15.6% in their cement volumes in the first 9 months of 2020 to 21.1 Mt/a cement from 17.8 Mt/a in the same period of 2019. The volumes decreased in Q1 of 2020 by -13.3% and in Q2 of 2020 by -33.3%, while in Q3 of 2020 a slight increase by +1.6% was recorded.

3 Profitability and M&A activities

Due to the Covid-19 impact the profitability of most cement companies decreased. However, despite lower net revenues, but with a disciplined cost management some of the TOP cement producers were able to generate positive results. A balanced cement portfolio helped to increase operating EBITDA and the EBITDA margins. Generally, producers with most of their portfolio in North Ameri-ca, Northern Europe, CEE and Africa have been able to improve their operating results, while producers with their portfolio concentrated in Southern Europe, India and other Asia Pacific countries (excl. China) ran into problems. Generally, regional players had larger problems than the international players with a more balanced portfolio.

Cement companies are often not only evaluated by their market capitalization, equity (total assets minus total liabilities), net sales and (recurring) EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization), but also by financial performance indicators (metrics) such as free cash flow, the Net Debt/EBITDA ratio, EBITDA margin, Return on Sales (ROS), Return on Equity (ROE) and Return on Capital Employed (ROCE). For most of the cement heavyweights, such as LafargeHolcim, HeidelbergCement, Cemex, CRH, Votorantim and Intercement, the net debt is much larger than the EBITDA, while a few, such as Buzzi Unicem and Dangote Cement, have a net debt lower than the EBITDA. To value the financial strength of a company, the free cash flow, net debt/EBITDA ratio and EBITDA margin are mostly taken into consideration.

In the capital-intensive cement industry, the net debt/EBITDA ratio is sustainable (tolerable) in a range of 1.0 to 2.4. However, many companies do not achieve this range and accordingly they are heavily in debt, with examples such as Cemex, Votorantim and Intercement. HeidelbergCement (Figure 14) reduced its net debt from € 10.439 billion in June 2019 to € 8.994 billion in 2020 and accordingly the net debt/EBITDA ratio was reduced below the internal 2.0x target, as it was in 2015 before the acquisition of the Italcementi Group. HeidelbergCement also limited CapEx at approximately € 1.2 billion and used cash flow generation and cash balances to repay maturing debt, leading to a significant deleveraging of gross debt.

In the last 5 years the cement sector has changed massively. The Top 10 cement producers in China now combine about 60% of the capacity, after about 30% in 2015. In the Rest-of-the-World the situation changed with the € 41 billion merger of Lafarge and Holcim in 2015 and the corresponding large divestment of cement assets by Lafarge and Holcim to the CRH Group, as well as the acquisition of Italcementi by HeidelbergCement. As a consequence of these deals, several divestments have been made by LafargeHolcim and Heidelberg-Cement in the years from 2015 to now. Worldwide, national and regional players have been able to increase market shares and some regional champions have emerged.

Some of the most commented asset divestments include those by LafargeHolcim to Semen Indonesia in Indonesia, to YTL in Malaysia, to San Miguel in the Philippines, to Siam City Cement in Thailand, Vietnam and Sri Lanka, those by HeidelbergCement to Argos in the USA, to Cementir in Belgium and to Buzzi Unicem and Colacem in Italy. CRH, which already substantially increased their portfolio after the takeover in 2015 of a € 6.5 billion “high quality package across 4 regional markets” from LafargeHolcim reached another agreement in 2017 to acquire Ash Grove Cement for a total consideration of US$ 3.5 billion. In 2019 CRH sold its 50% stake in India-based My Home Industries for US$ 354 million.

Cemex went heavily into debt with the acquisition of Rinker in 2007. Their net debt in that year increased from US$ 4.584 billion to US$ 18.904 billion and still stands at US$ 11.634 billion and a net debt/EBITDA ratio of 4.89x (2019). This very high leverage still exists after several asset-divestment programs and the divestment of USA assets to Eagle Materials, UK assets to the Breedon Group, Bangladesh assets to Siam City Cement, Baltic assets to the Schwenk Group and white cement assets with the exception of Mexico to the Cimsa Group. However, this is not the end of the divestments that have to be made by Cemex.

Intercement is another example in the cement industry of an excessively high net debt/EBITDA leverage. Accordingly, in 2019 the company divested its Portugal and Cape Verde cement assets to the Turkish OYAG Group (Ordu Yardimlasma Kurumu) for a reference price of about US$ 810 million. After this divestment, the net debt/EBITDA ratio of the company was still in the range of 4.5 to 5.5x, depending on the refinancing of the debts and the company’s agreements with the main lenders. However, with the sale of Yguazu Cementos in Paraquay and a positive development in the sales volumes, especially in Brazil, Intercement was able to reduce its net debt by 18.4% to US$ 1.309 billion at the end of Q3 2020.

OYAK is one of the examples of a fast-growing Cement Group. In the last three years the Group has expanded its cement capacities by 52%. These comprise the six cement subsidiaries Adana, Bolu, Aslan, Ünye, Mardin and Denizli (Figure 15) in Turkey, which have a combined cement capacity of 22.9 Mt/a, and 6.5 Mt/a from the acquisition in 2019 of the CIMPOR assets in Portugal and Cape Verde from Intercement. In 2020 the installation of a grinding plant in the Ivory Coast was completed. OYAK intends to implement its vision of becoming a global cement leader through the JV with Taiwan Cement Company (TCC), which has 11 Mt/a cement capacity in Taiwan and about 65 Mt/a in China. As a result of this JV, TCC has acquired 40% shares of OYAK Cimento for US$ 640 million. For TCC this is a pioneering step to expand outside the Asian market and the Chinese market, which is almost at saturation point.

Beside the above-mentioned M&A, many more agreements have been finalized in the last few years and many more will come. The deals include acquisitions by the HeidelbergCement Group including Elementia in the USA by Lehigh Hanson, Emirates Cement in Bangladesh from Ultratech as well as Newcomers Atlantic Cement and Cimsud in Morocco by Ciments du Maroc. Sibirsky Cement (SibCem) acquires a controlling stake in Angarskcement and Iskitimcement via Topkinsky Cement. Cementos Progreso completes takeover of Cemento Interoceanico in Panama. CRH has agreed to sell its Brazilian business to Companhia Nacional de Cimento (CNC), a joint venture between Italy-based Buzzi Unicem and Grupo Ricardo Brennand, for US$ 218 million. In India the Nirma Group has acquired the cement assets of Emami Cement.

There are also far more acquisitions of cement assets by Chinese companies to come, especially in Sub-Saharan Africa. Recent examples include the acquisition of ARM’s cement unit in Tanzania by Huaxin Cement, the proposed acquisition of Ohorongo Cement from Schwenk by West China Cement (a subsidiary of Anhui Conch Cement), which was finally blocked by the Namibian Competition Commission, and last but not least the acquisition of a stake in the Pemba cement plant in Mozambique by Sino Energy International. Due to stagnating cement markets in Japan, Taiheiyo is also looking for foreign investments. Taiheiyo has acquired a stake in one of Semen Indonesia’s subsidiaries. Furthermore, the two companies finalised a collaboration agreement with the aim of building a comprehensive partnership.

Another opportunity emerged in Russia via Sherbank, a state-owned Russian banking and financial services heavyweight. Sherbank has consolidated 100% of the shares of Eurocement Group from the former shareholder GFI Investment. The assets of Eurocement amounted to RUB 79.2 billion, which are now offered by Sherbank for sale. In 2014 Sherbank and Eurocement signed a cooperation agreement to modernise Eurocement’s cement production technology (Figure 16) by 2018 by completely converting to the “dry” method. Eurocement operates 19 cement plants in Russia, Uzbekistan and the Ukraine with a combined cement production capacity of about 60 Mt/a and more than 11 million m3 of concrete. From our point of view, the Eurocement assets will fit perfectly into the portfolio of a number of cement producers, including HeidelbergCement and Buzzi Unicem, who already focus on the CIS markets.

HeidelbergCement will divest assets which do not meet their investment criteria, to create more value through disposals. In a plan outlined in September on the Capital Markets Day 2020 it was announced that in the period 2021-2025 the amount of divestments will significantly increase when compared to the 2018-2020 period. The plan particularly includes a shifting from non-core to core asset disposals. The idea behind this is to simplify and prioritize the portfolio. All M&A will be on stringent investment criteria, which include a strategic fit, alignment with the portfolio strategy, a contribution to the net profit in 1 year after acquisition and last but not least, a ROIC (Return-On-Invested-Capital) clearly above 8% after full integration. Up to now, HeidelbergCement has operated 5.0 Mt/a cement capacity in Russia, which could generate synergy potential.

4 Climate change and resources

The reduction of carbon emissions has become one of the biggest challenges faced by the cement industry. The European cement industry, which is leading in this field, has reduced its CO2 emissions relative to 1990 by about 15%. For 2030 the gross emissions shall be reduced by 30% for cement and by 40% down the value chain, including concrete. In the Cembureau 2030 roadmap [3] the emissions have to be reduced from 783 kg CO2/t of cement to 472 kg CO2/t of cement down the value chain. Decarbonated raw materials, alternative fuels, higher thermal efficiency and low-carbon clinker shall contribute a reduction by 61 kg/t, while clinker substitution, electrical efficiency/renewables shall provide another 35 kg/t and finally the concrete mix and construction carbonation shall provide 99 kg/t CO2 savings.

According to research by the IVL Swedish Environmental Research Institute, about 23% of the process CO2 from the limestone calcination in cement kilns is being absorbed annually by the concrete in the built-up environment of our cities and infrastructure [4]. This process is called re-carbonation. It is comparable to the absorption of CO2 by the photosynthesis of plants and trees, with the difference that concrete stores CO2 permanently. Re-carbonation increases after demolition of a concrete structure, because recycled concrete has a higher surface area to absorb CO2 more easily. Using the exhaust gases from cement kilns can accelerate the re-carbonation of recycled concrete. Today it is already possible to make accurate estimations of the amount of CO2 absorbed by the building stock for a given country or region. The re-carbonation concept equates to 8% savings of total CO2 emissions from cement production.

In December 2020 the EU agreed on tougher climate goals for 2030. Instead of the envisaged 40% reduction compared to 1990, a reduction of the carbon emissions of 55% should now be achieved. It is too early to comment whether Cembureau will also adjust its roadmap. However, Europe will continue to lead carbon reduction measures. HeidelbergCement has set the industry-leading emission target of <500 kg CO2/t by 2030. By 2019 already 590 kg CO2/t had been achieved, which corresponds to a reduction of -22%, compared to 1990. Never-theless, Europe and the European based cement producers are not alone. Cemex achieved a CO2 emission reduction by 22.4% and has set a target of 35% by 2030. Votorantim Cimentos achieved 23% in 2019 and targets 520 kg CO2/t by 2030.

By 2050, the objective is to implement the concept of carbon neutrality of the cement and concrete industry, which is backed by most of the major cement producers and global cement institutions. This goal can only be achieved if carbon capture, utilisation and storage (CCUS) concepts are implemented. The different processes that can be used have to contribute in Europe to the reduction of about 42% of the emissions. Up to now only a few processes such as the Leilac-technology (Figure 17) are at an advanced technical readiness level (TRL). The problems of all the technologies are the high operational and investment cost, which will have a significant impact on the cement production costs [5]. Cembureau projects a reduction of the clinker factor in cement from about 77% to 74% in 2030 and 65% in 2050. However, the reduced availability of resources such as granulated blast furnace slag and fly ash is problematic [6].

5 Market outlook

The cement industry is optimistic that a significant recovery of the cement volumes will be achieved in all world regions in 2021, despite the continuing Covid-19 pandemic. The global outlook for 2021 and beyond will very much depend on the development in China. OneStone is projecting a massive decline in China of just about 70% of the 2019 production levels by 2030. For the Rest of the World an increase of 27% by 2030 is projected, with the largest increases in South Asia (+59%) and Latin America (+32%). The recovery of cement volumes in the short-term will help the cement producers to become more profitable. After the pandemic there will be more cement companies which have based their capacity expansion projects on market growth, but whose lower net income will no longer allow them to service their liabilities. Another aspect has become obvious: cement producers need to exceed a critical size, which is necessary in order to generate cash to cover a downturn and to fulfil other challenging restrictions.